Steady progress continues for Phoenix Mills on all fronts:

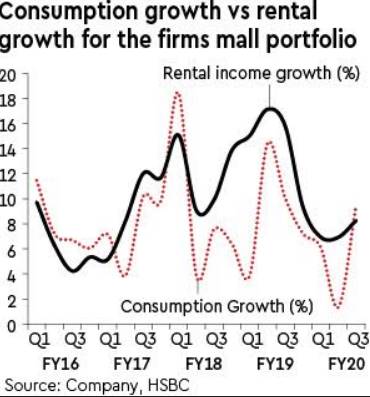

(i) Consumption growth in portfolio malls remains in high single digits in the current quarter;

(ii) five malls are under construction; one of these, in Lucknow, is due to commence trading by mid-March while the other four will be commissioned over the next four years. Pre-leasing momentum is strong for these, with at least three having already pre-leased c40% of space; (iii) with c60% of total mall area up for renewal during FY20-22, the company continues to see a steady uptick in rental values during renegotiations ; (iv) the company has a pipeline of new tenants that are yet to find a place in its malls.

Investment view: We expect the market city malls to gradually make their way along the premiumisation curve, facilitated by rental renewals due over the next three years. We expect rental growth to remain strong on ramp-up of Palladium, Chennai, and start of Lucknow mall. This should drive consolidated rental growth of 15% over FY20-25e vs 11% during FY14-19.

Valuation and risks: We use a sum-of-the-parts DCF methodology to value the cash flows from assets, to arrive at fair value as of Mar’20e. We lower our weighted average cost of capital to 11% from 11.6% as we incorporate our new cost of equity assumptions, which results in a new target price of Rs 1,110 (earlier Rs 1,000).