Weaker volumes in India/Europe and higher costs in TCNA impact operating performance

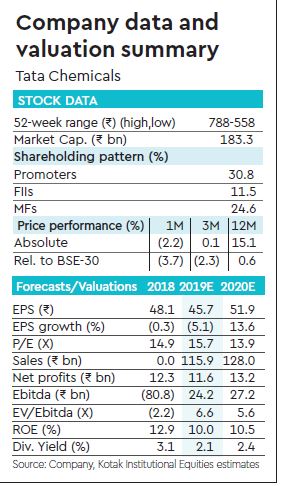

Tata Chemicals (TTCH) reported weak results in Q4FY18 with 9% q-o-q decline in Ebitda to Rs 5.1 bn led by 4% q-o-q decline in India soda ash volumes, 25% q-o-q decline in Europe volumes and escalation in costs for North American operations. Higher other income and lower interest cost led to 1% q-o-q increase in PBT and boosted reported net income to Rs 15.8 bn.

Modest ex-salt consumer revenues of Rs 1 bn: TTCH’s ex-salt consumer revenues fell to Rs 1 bn in FY2018; salt revenues increased to Rs 17-18 bn amid stable volumes at 1.02 mt. The management reiterated its guidance of growing consumer business revenues to Rs 50 bn over the next 4-5 years.

Deleveraging largely over

Consolidated net debt reduced to Rs 18.6 bn as of March 31, 2018 from Rs 56 bn a year ago led by the sale of urea operations and improvement in working capital due to a reduction in subsidy receivables. TTCH’s balance sheet is expected to improve further during the fiscal year on receipt of Rs 3.8 bn pertaining to sale of phosphatic fertiliser business and Rs 8.6 bn of subsidy receivables.

3-5% increase in EPS estimates

We raise our FY2019-20 EPS estimates by 3-5% factoring in (i) improved outlook of global soda ash business, (ii) modestly higher other income and lower interest cost, (iii) details of FY2018 balance sheet and (iv) other minor changes. We retain Add rating with TP of Rs 760 based on March 2020e estimates given reasonable valuation.