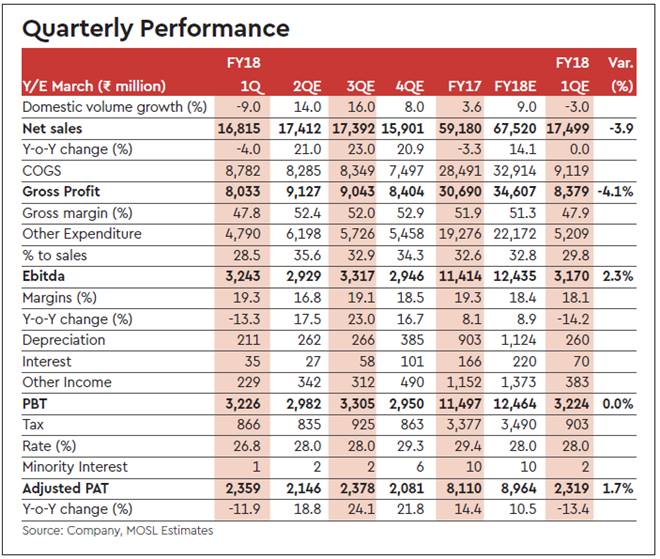

Marico posted 4% y-o-y decline in consol. net sales (est. flat sales) to Rs 16.8 billion. Domestic volume decline was 9% y-o-y (est. of -3%), while revenues fell 4%. International revenue grew 6% y-o-y with 1% overall sales decline. Rural sales declined 11%, while urban sales were flat ahead of GST roll-out. Modern trade (10% of India turnover) grew 11% y-o-y. Management attributed sales and volume decline to pipeline issues. CSD (7% of domestic sales) declined 15% y-o-y in 1QFY18. The company increased market share in all categories. Consol. gross margin shrunk 430bp y-o-y (est. of -400bp) to 47.8%. Copra costs rose 69% y-o-y and 7% q-o-q. Rice bran oil price was down 5% y-o-y, while liquid paraffin (LLP) price was up 21% y-o-y.

HDPE (a key ingredient in packaging material) price was down 4% y-o-y. Gross margin contraction can be ascribed to delay in price increases because of GST implementation. Consol. A&P expenses declined 230bp y-o-y and 22.9% on absolute basis y-o-y. There was a decrease in other expenditure by 40bp y-o-y, while staff costs increased 50bp y-o-y. EBITDA margin contracted 210bp y-o-y (lower than est. of – 300bp) to 19.3%, and thus, EBITDA fell 13.3% y-o-y (est. of -14.2%) to Rs 3.24 billion. Adj.

PAT declined 11.9% y-o-y (est. of -13.4%) to Rs 2.36 billion, 1.7% ahead of our estimate. Segmental growth: Parachute sales grew 3% y-o-y with 9% volume decline (est. of mid-single-digit volume decline); Saffola sales declined 8%, with volume decline of 8% (est. of mid-single-digit volume decline); and Value Added Hair Oils (VAHO) sales declined 8%, with 9% volume decline (est. of mid-single-digit volume decline). The Youth brands portfolio declined 23% in value terms. We currently have a Neutral rating on the stock.