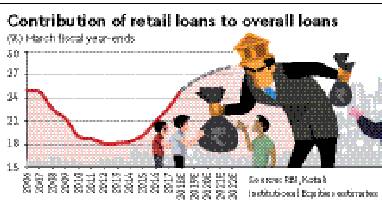

Retail loans now account for a fourth of all loans, an all-time high. However, a big chunk of this or close to one-third are estimated to be unsecured loans or those which banks have given without holding any collateral. These comprise loans for consumer durables, credit card outstandings and what the Reserve Bank of India (RBI) categorises as “other personal loans”. Typically, retail advances other than housing loans, vehicle loans, loans against deposits and other financial instruments, and education loans are deemed unsecured. The RBI shows that at Rs 18.54 lakh crore, outstanding loans to individuals constituted over a fourth of overall bank credit, which stood at Rs 73.74 lakh crore as on February 16.

Analysts attribute the rising trend in unsecured loans to the stiff competition in the home loan markets where non-banking financial companies (NBFCs) are making inroads; the portfolio of the top 10 NBFCs at the end of December 2017 was `56,200 crore or about 36% of all mortgages.

While home loans given by banks grew as much as 16% year-on-year, in September 2016 this decelerated to a single digit. While mortgages continue to contribute half the value of retail loans — 51.5%, to be precise — this marks a 200-basis point fall from what it was in February 2016.

Meanwhile, lending to micro and small and medium enterprises has picked up in the nine months to December 2017; while outstanding micro and small loans grew at 4% year-on-year, loans to medium-sized companies grew at 2.3% year-on-year. In fact, loans to large companies too grew by a small 0.4% year-on-year.

State Bank of India chairman Rajnish Kumar said recently the lender was being selective about corporate borrowers, with the emphasis more on retail lending, including SME.

At Bank of Baroda, the share of retail assets rose to 22% from 19% between December 2016 and December 2017.The management said housing loans have been a key driver of growth, up 44.3% in Q3FY18, as had auto loans.