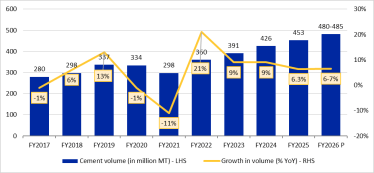

Cement volumes are expected to expand by 6-7 per cent in FY2026, stated a report by ICRA. This, it added, will be driven by a projected pick-up in demand from the housing and infrastructure sectors, following a growth of 6.3 per cent in FY2025. Despite global uncertainties, capacity addition in the cement sector is projected to increase to 43- 45 million MTPA in FY2026, up from 32- 35 million MTPA in FY2025. ICRA continues to hold a stable outlook for the industry.

In H1FY25, volumes had gone up by a modest 1.7 per cent YoY to around 212 million MT, primarily due to the slowdown in construction activity owing to the General Elections, the extended monsoons during H1FY25 and overall slowdown in private capex. However, in H2FY25, cement volumes witnessed a healthy growth of 10.7 per cent YoY to around 241 million MT driven by pick-up in construction activity. On the back of the healthy demand prospects, cement companies are expanding their capacities, both through the organic and the inorganic route, to further strengthen their market share.

Abhishek Lahoti, Assistant Vice President and Sector Head, Corporate Ratings, ICRA, said, “Backed by healthy demand, ICRA foresees a capacity addition in the cement industry of 43-45 million MTPA in FY2026, rising from the estimated addition of 32-35 million MTPA in FY2025.”

During FY2026, per ICRA analysis, eastern and northern India are likely to lead the grinding capacity supply, together adding 22-24 million MTPA, largely equally split between the two regions. The southern region, despite an oversupply of capacity, is experiencing significant capacity additions by large cement companies as it is operating at optimal utilisation levels and intends to maintain its market share in the near term. Abhishek Lahoti added, “Overall, the industry’s capacity utilisation is likely to remain stable at 70 per cent in FY2026, similar to FY2025, on an expanded base.”

Cement prices recovery

The cement prices have shown some signs of recovery from Q3 onwards with pick-up in demand, after witnessing 10 per cent decline in average realisation during H1FY25. While lower realisation has impacted profitability during FY25, moderation in costs of coal and pet-coke, which declined by 23 per cent and 13 per cent YoY, respectively, provided some respite to cement companies in the interim.

“The credit profile of cement producers, especially of larger and mid-size companies, is expected to remain stable, driven by a healthy growth in operating income, expected improvement in operating margins and comfortable leverage metrics. However, smaller players will witness pressure on their credit profile in the backdrop of moderation in operating profitability. Consolidation in the Indian cement industry has constrained pricing flexibility of small/regional players, which will weigh on their profitability in the medium term,” Abhishek Lahoti added.