")

In March, 2016, an embattled Tata Steel was all set to pull out of its bleeding UK operations. The company’s board had rejected an “unaffordable” turnaround plan for Port Talbot and instead greenlighted a sale of its UK operations. This was nine years after it had bought Corus for $12.9 billion, becoming Europe’s second largest steelmaker. At the time, Port Talbot, Britain’s biggest steelworks, was losing an estimated million pounds a day and was unlikely to find a buyer.

Earlier this month, the British government agreed to fund about 40% or £500 million of the total cost of £1.25 billion, to replace the existing blast furnace in Port Talbot with a new 3 million tonnes per annum electric arc furnace. The new plant will have significantly lower carbon emissions, down to 0.4 tonnes Co2e per tonne of steel from 2.16 tonnes currently. Operating costs are expected to come down to £160-170 /tonne once the new plant is commissioned.

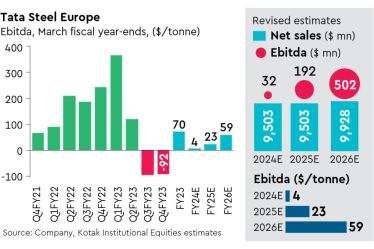

Experts believe that the new project could bring down the UK operation’s losses sustainably. “This is a step in the right direction and we would revise our earnings and cash flows after getting more details,” analysts at Kotak Institutional Equities observed.

In the past, steelmaking in the UK has been badly hit for several reasons including cheap Chinese imports, high energy costs and tepid demand. Not so long back, Tata Steel had cautioned that the finances of its UK business face “material uncertainty” given market conditions and the level of government support. A stress test of its European arm to assess the impact of a downturn had flagged concerns for the UK unit, the company had indicated. However, it was hopeful things would get better. Although the world economy is slowing and Europe and China in particular could take time to recover, the outlook for the steel market in the UK seems good.

One of the reasons for that is the demand in the UK market, which is reasonably good at 9 million tonnes per annum(mtpa). Tata Steel commands a fairly large share of 40-50% across segments such as auto, construction and packaging. Moreover, the company can also export scrap of about 10 mtpa.

The UK government’s grant of £500 million, analysts believe, could lower the losses of the UK operations meaningfully. It’s critical the operations become viable because Tata Steel Europe’s finances have been precarious for many years now after the Corus buyout in 2007, which raised Tata Steel’s indebtedness significantly. At one point, Fitch had downgraded the long-term rating to ‘AA’ from ‘AAA’, citing a sharp correction in global demand for steel products. In May, 2009, the company entered into talks with lenders to amend loan covenants to avoid a possible covenant breach in the second half of 2009, rating agency Standard & Poor’s had said, citing the company’s management. The agency red-flagged a downgrade of Tata Steel UK’s senior secured debt.

The business has consistently lost money. Many years after the acquisition, the losses continue to pile up. From `3,955 crore in March 2015, for instance, consolidated losses rose to `4,169 crore in March, 2017. While it was never mentioned publicly, at one time, the company was bracing for huge writedowns of over $10 billion. On several occasions, attempts were made to sell the facilities. Attempts have also been made to try and exit, or partially exit, some businesses. In March, 2016, the company announced plans to sell its UK steel assets, including the Port Talbot unit in a bid to cut losses that had been going up because of a crash in steel prices and competition from cheap imports. The decision put some 15,000 jobs at risk. Soon thereafter, the company initiated talks with Germany’s Thyssenkrupp AG to merge its European steel business.

In June 2018, they signed definitive agreement to combine their European steelmaking businesses in a 50-50 joint venture in a new company. However, about a year later in May, 2019, they abandoned the ambitious merger after the European Commission nixed the deal saying it could result in significant price hikes and demanded remedies.

Tata Steel Europe has also been grappling with pensions, and was in discussions with the British Steel Pension Scheme trustee and the pension regulator to develop a structural solution for its UK pension scheme. Recently, it divested its remaining 40% ownership in the £12 billion pension portfolio completely de-risking the company’s exposure. According to Koushik Chatterjee, chief financial officer of Tata Steel, this has been one of the most significant and complex de-risking projects for Tata Steel. The revamp of Port Talbot could be a turning point for the company. For most part of the last decade the Netherlands business has been profitable both in terms of earnings and the cash flows. However, due to structural issues, the UK hasn’t been profitable or able to meet its own cash requirements.

“Now with this announcement and the project we propose to reboot the UK business to a new phase,” Chatterjee said. The company is working to resolve the structural weakness, put in place state of the art facilities, improve productivity. “We are working to lower the cost base and drive efficiencies through more automation and digitisation. The business model will be more customer-centric,” he added.

Once the EAF project is completed and commissioned, the company is confident the UK business will be profitable. Shareholders will look forward to that.