Biocon and partner Mylan launched Semglee (insulin glargine) in the US (reference drug: Sanofi’s Lantus, annual US sales ~$2.2 bn). The US FDA approved Semglee on 11 June 2020 as a “follow-on-biologic (FoB)” to Sanofi’s Lantus brand and for the same indications (Type 1 diabetes in adults and paediatric patients and Type 2 diabetes in adults). Semglee will be available in vial and pre-filled pen (Basaglar, competing FoB from Eli Lilly & Boehringer Ingelheim, is available only as pre-filled pens).

Mylan continues its discussion with FDA to obtain an ‘interchangeable’ designation for Semglee, which if received could help in automatic substitution of prescriptions with Lantus at formularies.

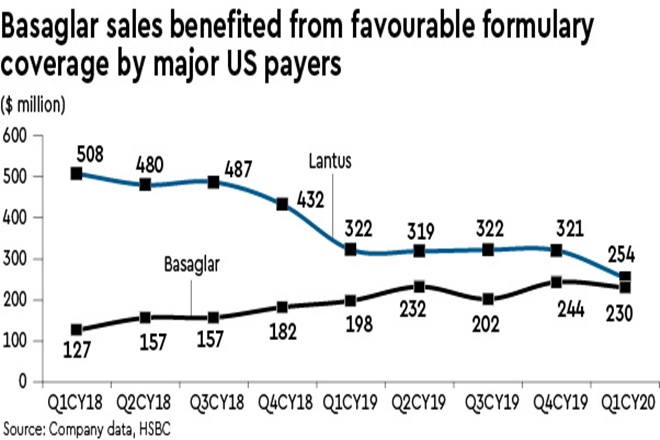

Gaining favourable formulary coverage is key: Semglee is one of the most critical launches for biosimilars from the Biocon/Mylan partnership: they look well prepared to monetise opportunities in the US. Biocon has manufacturing capacity for Semglee at its insulin plant in Malaysia to cater for market demand. The insulin glargine market in the US is significant, with $1.3-bn sales for Lantus and $876-m for Basaglar in CY2019.

Biocon’s supply agility and pricing of Semglee are key in gaining wide formulary coverage by payers in the US. Biocon/Mylan launched Semglee at a wholesale acquisition cost (WAC) of $147.98 per package of five 3ml pens and $98.65 per 10ml vial, representing the lowest WAC for any long-acting insulin glargine in the market. We see opportunity for Semglee amid increasing US demand for cheaper insulin products, and prudent execution should help it gain good share of the glargine market.

Buy, Rs 475 TP: Despite near-term volatilities, Biocon is well placed to benefit from a favourable push for biosimilars on the back of a strong pipeline and proven capabilities. It has good visibility on biosimilar catalysts, e.g. (a) significant pick-up in sales of launched biosimilars in the US and EU over the next few months; and (b) expected approval of biosimilar bevacizumab in the US and EU.

Semglee sales scale-up in the US should help in cost break-even for its Malaysia insulin near-term, helping operating margins. We maintain our estimates, Rs 475 TP and Buy rating.