Reports of a government-sponsored Asset Reconstruction Company (ARC) with a corpus of some R50,000 crore being created to bail out state-owned lenders by buying up their toxic loans seem completely out of sync with the state of the government?s finances.

The government has been hard?pressed to capitalise state-owned banks, infusing barely R15,000 crore last year against demands that were three times higher; taking over the toxic loans at a small haircut would help free up resources for banks, but that?s a bad idea. A better way to use the money would be to identify some of the larger critical projects and help financial closure through some equity support; with the government becoming an equity shareholder in these ventures, they should hopefully get off the ground faster and, once cash flows start coming in the banks will be repaid. If, in the process, the private shareholders get diluted or even bought out, so be it. It makes sense to push ventures that are already on the drawing board than to hand out cash to banks to lend elsewhere.

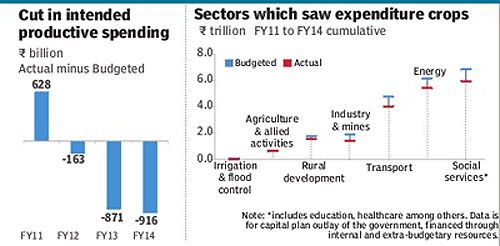

The fund can be created through a budget allocation to capital expenditure, which as a share of total expenditure, has been slipping steadily over the years; from 23% in 2005, it dropped to17% in 2008 and further to 10% in 2009, before recovering to 12% in 2012. Indeed, an initiative of this nature where the government targets spends on select projects will be very effective in supporting the investment cycle. Even if, in the process, there is some overshooting of the fiscal deficit target of 4.1%, as planned for in the interim budget, it would be worth the expenditure.

Ideally, the government should not be ?taking over? projects that have been promoted by the private sector. Unfortunately, however, over-leveraged private sector promoters have not been able to deliver on their commitments. Not all the fault is theirs; it is true that several projects are stuck because the necessary clearances and linkages haven?t come through in time. But there are several that aren?t taking off because promoters simply don?t have enough funds but are loathe to diluting their equity. So if concessionaires have walked out of road projects on the grounds that NHAI hasn?t delivered the environmental or forest clearances in time, they?re only partly justified in doing so; the fact is they are uncomfortable pursuing the projects that are no longer viable.

CRISIL, for instance, has pointed out that five out of a clutch of six road projects, for which base traffic has been lower by 20-40% and the average cost overrun is 23%, could be in trouble. The rating agency finds that that the projects have an average debt-service coverage ratio of less than one, in the first five years of operations, which means that if no additional capital is infused, developers will find it difficult to service the loans.

The way to approach these projects would be first to re-work them with realistic assumptions for both costs and revenues and, thereafter, bridge the equity gap. The higher equity component will comfort banks even if the asset is classified as sub-standard because of the commissioning delays. It is not as though the government needs to hold on to these stakes forever; once the cash flows start coming in, these can be offloaded to Private Equity (PE) funds who will be willing buyers. In fact, once it is clear that equity will be pumped in and the project re-worked, funds will move in if the valuations are attractive enough. And once the venture stabilises even banks will not find it difficult to sell the loans to new lenders; hopefully in a few years, a fair amount of take-out financing or investments from Infrastructure Development Funds (IDF) will be in place to buy the loans from banks.

No doubt banks? balance sheets will be strained till they are able to offload some of their stressed infra assets but this is the price they have to pay for teaming up with the wrong promoters and not having done enough due diligence. There can be no justification for banks having lent thousands of crores to promoters whose companies earn revenues only of a few hundred crores except that they didn?t do their homework. Taking over their bad loans amounts to a bailout which they don?t deserve.In the past two years, there has been a sharp cut in the government?s productive spends which includes the Centre?s capital expenditure and the revenue grants it gives for capital creation; the target for FY14 was 1.7% of GDP or less than R2 lakh crore. A project restructuring company (PRC) could be a focussed way of increasing capital spends. A PRC is what the economy needs right now, not an ARC.

shobhana.subramanian@expressindia.com