The Modi government managed to bring together states of various political hues for the Goods and Services Tax (GST) by finding the middle road in administrative power-sharing via the mechanism of the finely balanced Centre-State GST Council. The guaranteed 5-year compensation for ‘revenue shortfall’—defined against 14% annual increase over FY16 base – also helped to overcome some states’ reluctance to embrace the epochal indirect tax reform.

If nineteen months since its launch the GST has yet to stabilise and is struggling to produce the revenue buoyancy and incremental economic efficiency it is theoretically capable of, it is not only due to the inevitable teething troubles that such a big change would have anyway created, but also because of the multiple structural deficiencies the new tax was born with.

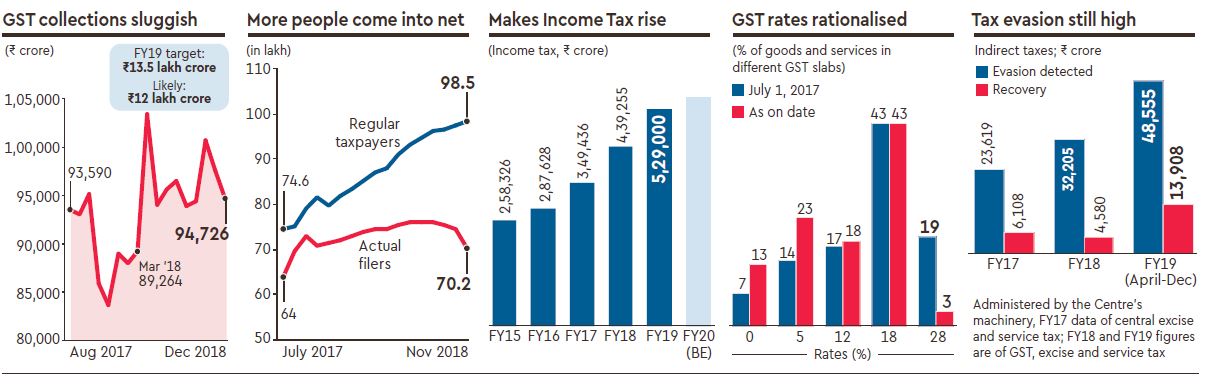

Far from the simple, one-nation-one-tax envisaged by experts, India’s GST came into being with practically seven or more rates and excluding many high-revenue-earning segments (chiefly, petroleum products namely diesel and petrol, real estate and alcohol, the last excluded even constitutionally, the others with a promise to include later). Also, the input tax credits were not released to the businesses promptly, leading to serious working capital problems for small units.

The rates were initially high (28%) for a wide array of consumer articles. The small services industry, which was used to benign rates, has reeled under an 18% GST. A large segment of MSMEs has found GST compliance cumbersome, especially since it closely followed the note ban. To top it all, a foolproof returns-filing system has got deferred several times and not in force even now, undermining tax officials’ ability to undertake invoices-matching and check evasion. (The latest word is that a beta version of a simplified system will start running by April).

Of course, the GST Council, often at the initiative of Union finance minister Arun Jaitley, has over the last several months taken a number of steps to improve the GST structure. Rates were cut for nearly 120 goods and services since July 2018 itself; as a result, the highest slab of 28% GST is now restricted to only 37 items or 3% of total items under GST. The weighted average GST rate is, however, still higher than most countries with similar multi-point tax on value addition.

Recently, the GST exemption limit was raised from Rs20 lakh to Rs40 lakh, the threshold for the composition scheme—which allows tax payment as a tiny fraction of turnover rather than transaction-wise—was enhanced to Rs1.5 crore from Rs50 lakh, and the facility got extended to service-sector players with up to Rs50 lakh annual sales. From April this fiscal, e-way bills have got rolled out in phases across the country, for moving consignments worth over Rs50,000 (staggered enforcement of mandatory radio frequency tags on vehicles has, however, been problem, leading to excessive manual supervisions).

While these steps may address the woes of aggrieved taxpayers, some of them—like an option for states to keep the exemption limit between Rs20 lakh and Rs40 lakh and permission to Kerala to have temporary calamity cess—go against the idea of flawless GST.

There is talk of GST revenue shortfall for the Centre—overall (Centre-state) mop-up for April-December this fiscal was Rs96,800 crore/month, much below Rs1.1 lakh crore/month or thereabouts needed for the Centre to meet its budget estimate including the compensation cess proceeds. There is of course a gradual rise in revenue—this fiscal’s average monthly collections are up 8% over last year’s. What augurs well for GST are some recent assertions by Jaitley and the Congress party’s proclaimed preference for a more inclusive GST with fewer rates. Jaitley said: “We are close to completing the first set of rates of rationalisation, i.e., phasing out the 28% slab except in luxury and sin goods. The country should eventually have a GST which will have only slabs of zero, 5% and standard rate (between 125 and 18%) with luxury and sin goods as an exception.”