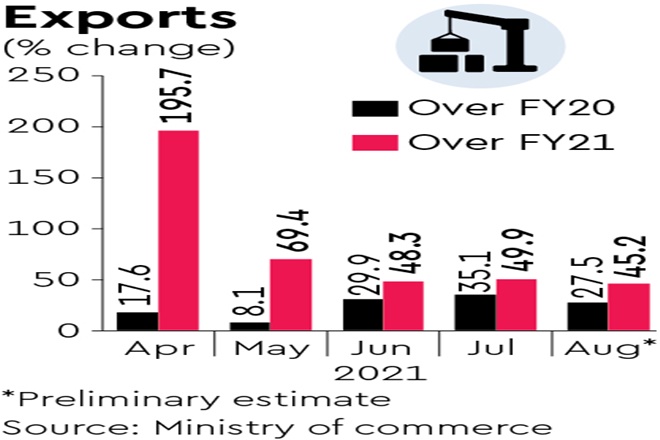

Merchandise exports surged 45% in August from a year before and over 27% from the pre-pandemic level (same month in FY20), buoyed by an economic resurgence in advanced markets and elevated global commodity prices.

Imports, too, jumped over 51% from a year earlier and 18% from the pre-Covid level, signalling a broader trade recovery. Goods exports have now crossed the pre-Covid level for six months in a row.

Exports in August touched $33.1 billion, while imports stood at $47 billion. Given the elevated imports, trade deficit hit a four-month high of $13.9 billion. Outbound shipments in the first five months of this fiscal rose to almost $164 billion, recording a jump of 67% y-o-y and 23% from the same period in 2019.

Commerce secretary BVR Subrahmanyam exuded confidence that, given the robust growth so far, the country will achieve the ambitious export target of $400 billion for FY22. Last fiscal, India could ship out goods worth only $291 billion due to the Covid outbreak.

Of course, as analysts have pointed out, export growth had remained subdued even before the pandemic — outbound shipments rose about 9% in 2018-19 but again shrank by 5% in 2019-20. So, only a sustained uptick over the next few years would help India recapture the lost heights. Importantly, core exports (excluding petroleum and gems and jewellery) shot up by 32% in August from a year before, lower than the 45% growth in overall merchandise exports, mainly due to a rise in global crude oil prices and resurgence in gems and jewellery exports after last year’s setback. Still, the growth remains encouraging, given the supply challenges posed by Covid.

Similarly, core imports rose 34% y-o-y and 3% from the level witnessed in August 2019. Overall, goods imports in April-August stood at $220 billion, up 82% from a year ago but only over 4% from 2019.

Among the key performers on the export front, outbound shipment of petroleum products surged by 140% in August, gems & jewellery 88%, engineering goods 59%, cotton yarn, fabrics, made-ups and handloom products 56% and electronics 31%. Similarly, imports of iron and steel jumped by 108% in August, followed by pearls, precious and semi-precious stones (93%), gold (82%) and petroleum (80%).

A Sakthivel, president, FIEO, stressed that many labour-intensive sectors were major contributors to the robust performance, which itself is a good sign as it will further help job creation. However, imports clocking $47 billion, with a year-on-year surge of 51% in August should be analysed, he added.