By Vinayak Chatterjee

The revival and growth of the Indian economy depends substantively on infrastructure investments. In this context, three questions assume pertinence: What is the desirable level of investment? Is there the financial capacity to fund this? And, is there an adequate pipeline of projects for the investment target to be met?

On the desirable level of investment, there appears to be a consensus that India should aspire to invest at least 8% of its GDP on infrastructure. That this is possible was shown in 2011, when GCFI (Gross Capital Formation in Infra as a percentage of GDP) hit 8.2%. The projected nominal FY24 GDP is expected to be ~Rs 285 lakh crore. So, an 8% GCFI would be ~Rs 23 lakh crore. This is consistent with the five-year target of Rs 111.3 lakh crore set in the National Infrastructure Pipeline (NIP) document. It is thus quite appropriate to take a figure of Rs 22 lakh crore per year, in the short term, as India’s desirable infra investment target.

For the second question, consider the availability of these financing buckets: Union Budget FY23 (Rs 7.5 lakh crore), states (Rs 6 lakh crore), PSUs and extra-budgetary resources (Rs 2.5 lakh crore), NaBFID (Rs 2 lakh crore), and private capital, domestic and foreign (Rs 4 lakh crore). These add up to Rs 22 lakh crore. So, India has the ability to fund around Rs 22 lakh crore on an annual basis.

The third question is the hardest to answer. At a conceptual level, the available infra project pipeline should be 4X the annual projected investment level because, from concept to commissioning, an infra project typically takes about four years. Therefore, a Rs 22-lakh-crore annual investment target needs Rs 88 lakh crore of ready investible projects. Does India have a Rs 88-lakh-crore “shovel-ready” project pipeline?

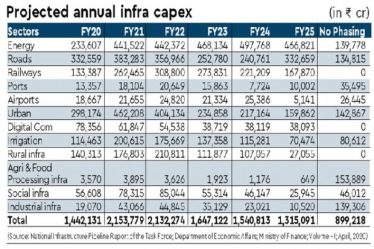

The April 2020 Report of the Task Force on National Infrastructure Pipeline offers the most credible answer. NIP has aggregated information from ministries, departments, states, and the private sector and has sought to capture all projects costing more than Rs 100 crore, whether under conceptualisation or construction (greenfield and brownfield). The accompanying graphic shows the sector-wise availability of investible projects.

The data reveals a pipeline of projects totalling around Rs 75.33 lakh crore over FY22 to FY25. However, the pipeline starts diminishing FY23 onwards. Also, Rs 9 lakh crore of projects listed under “No Phasing” suggests some ambiguity and uncertainty about their existence. While new projects will obviously get added each year, there is serious concern about stalled and delayed projects. As per Mospi data from December 2021, of 1,679 central sector projects (each costing Rs 150 crore or more), 11 are ahead of schedule, 292 are on schedule, and 541 are delayed, while neither the year of commissioning nor completion time is available for the remaining 835. The report also points out that the total original cost of implementation for the 1,679 projects was Rs 22.30 lakh crore, but now the anticipated cost is ~Rs 26.68 lakh crore—a cost overrun of Rs 4.38 lakh crore. A GAP ANALYSIS of the project pipeline availability versus the expectation over FY23-FY25, taking into account current visibility, ambiguous projects and potential for delays/stalling, puts the figure at ~Rs 34 lakh crore. So, if India is to sustain a Rs 22-lakh-crore infra-investment target in the here and now, and scale up to Rs 30 lakh crore in the medium term, then a fresh burst of project creation activity has to begin now, to generate a fresh pipeline of around Rs 50 lakh crore.

Infra-projects typically go through four stages: conceptualisation and in-principle clearances, development (detailed project reports, alignments, etc), closure (permissions, land acquisition, financial arrangements, etc), and construction and pre-ops. Meeting the investment targets requires “shovel-ready” projects—in other words, a meaningful fourth-stage bucket. To ensure that this “shovel-ready” bucket is available at the levels required, we need to work on and monitor the preceding three stages. This brings to the fore two operational requirements: One, the NIP document has to be aggressively pushed and refreshed every six months to boost confidence in the adequacy of project pipeline; and two, a group, possibly the GatiShakti team, now needs to create these four buckets, populate them, and highlight the required inferences. The narrative is clearly shifting from funding adequacy to project pipeline creation.

The author is Infrastructure sector expert and chairman, CII’s National Council on Infrastructure

Views are personal