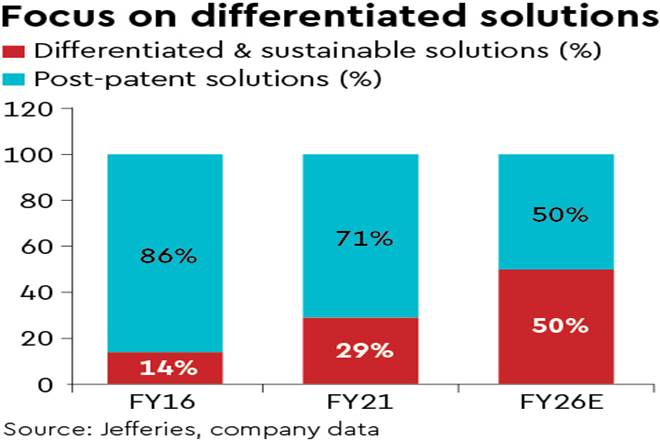

UPL’s FY21 Annual Report delves deeper into its key strategies for driving the next growth phase. UPL envisages to grow margin-accretive Differentiated Solutions from 29% of sales now to 50% by FY26. Innovation rate could rise to 30% over 3-5 yrs (21% now), thus enhancing product line. ESG focus continues, with robust sustainability goals by 2025. Synergies on track. UPL expects Net D/Ebitda at <2x by Mar’22 (JEFe at 1.7x). Buy. PT `965 (target PE at 14x).

Focused approach: UPL intends to focus on three key strategies: (i) Increase share of margin-accretive Differentiated Solutions from 29% of sales to 50% by FY26. (ii) Increase Innovation rate to 30% over 3-5 yrs from 21% in FY21, thereby enhancing product line. (iii) With 15 molecules in development pipeline, UPL envisages to achieve risk-adjusted revenue of $2.5 bn in next 5 yrs by leveraging collaboration to access new technology (e.g., Open-Ag, R&D). For FY21-24e, we estimate sales/PAT CAGR at +9%/ +23%, with op margin at 23.5% by FY24e (+140 bps), aided by improving mix and Arysta synergies.

ESG: UPL is strengthening focus on ESG, with 29% of sales now from differentiated & sustainable solutions. Also, company has achieved reduction in water consumption, carbon emission, and waste disposal across manufacturing operations over past 5 years; 50,000m3 of rainwater is harvested & reused annually. UPL’s cumulative sustainability loan is at $750 mn as of Jun21.

India’s growth outpaces: UPL’s FY21 sales split: (i) Lat-Am Rs 149 bn (+8% y-o-y). Growth despite forex devaluation in Brazil. (ii) N-America Rs 57 bn (+1%); supply constraints impacted Q4 sales. (iii) Europe Rs 64 bn (+12%); growth led by new product sales. (iv) RoW Rs 70 bn (+3%); strong growth in Asia, whereas flattish in Africa. (v) India Rs 47 bn (+22%). Favourable weather and new launches aided growth. Even in Q1FY22, India sales grew by +27%, led by favourable commodity prices (+14% for food grains, 36-48% for cash crops, pulses, etc.).

Debt reduction; synergies on track: Net debt reduced to Rs 189 bn in FY21 (Rs 201 bn in FY20), with Net Debt/ Ebitda at 2.2x. UPL replaced $500 mn acquisition loan with sustainability loan in FY21, with 30bps lower interest and extended maturity by 2 yrs.

Management expects Net D/Ebitda at <2x by Mar’22. Post Arysta acquisition in Feb’20, UPL has achieved revenue synergies worth $203 mn in FY21 — cumulative at $443 mn. Cost synergies at $126 mn in FY21, total at $235 mn.

Outlook, Buy: UPL’s growth prospects appear sturdy, with deleveraging, differentiated solutions (margin-accretive), strong crop prices, and launch of new platforms (NPP & nurture.farm). Retain Buy with PT of Rs 965. Target PE at 14x, broadly in line with historical 5-year average. Key risks: Global disruption, pricing pressures, and missing deleveraging target.