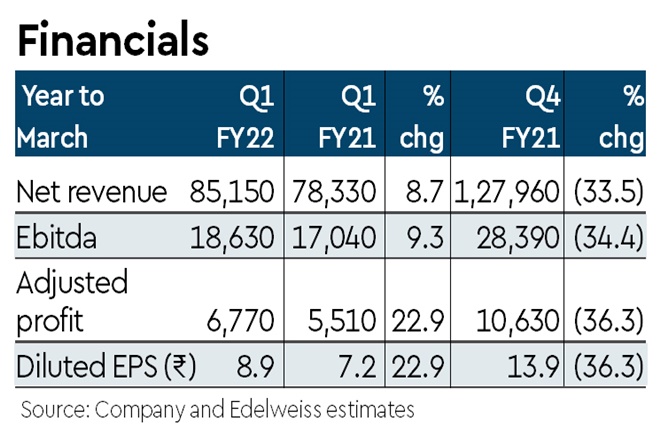

UPL delivered broadly in line Q1FY22 numbers with revenue growth of 9% y-o-y (est.10%) driven by 6% volume and 2% price rise. While India, Brazil and North America clocked strong growth, unfavourable climatic conditions impacted Europe and ROW growth. Improvement in product mix and better realisation helped the company deliver Ebitda growth of 9% y-o-y with stable margin of 22%.

Though it maintained FY22 guidance of 12-15% Ebitda growth, we believe favourable agri commodity prices will sustain the momentum. Hence, we have revised our target multiple to 18x (20% premium to 5-year average of 15x) yielding revised TP of Rs 1,019. Maintain Buy.

Volume spurt in major markets sustains earnings growth: UPL reported 9% y-o-y revenue growth to Rs 85 bn driven by favourable agri scenario across Indian and global markets. Volume growth of 6%, despite weakness in European markets, highlights the upward trend in the agri sector. UPL posted 24% y-o-y growth in LATAM markets. North America reported 19% growth driven by increase in crop acreage across row crops. Indian markets clocked 24% y-o-y growth led by higher price realisation. Europe remained a key drag with revenue declining 11% y-o-y primarily due to unfavourable weather scenario.

Mgmt maintains guidance: UPL has maintained its guidance for achieving revenue growth of 7–10% and Ebitda growth of 12-15%. We believe agri dynamics remain favourable driven by remunerative crop prices. The company’s net debt position as of June 2021 stands at Rs 215 bn. Working capital days increased by 7 to 91 days primarily due to higher inventory across plants ensuring adequate availability of raw materials. UPL expects to keep its net debt/Ebitda below 2x by March 2022.

Outlook: Favourable tailwinds– UPL has been one of the major players in the global agrochemical market. The company is well placed to reap benefits of strong sector tailwinds, which will drive Ebitdagrowth above 10% during FY22. We maintain Buy with revised TP of Rs 1,019 (earlier Rs 850) at 18x Q2FY23e EPS.