in the wake of a disappointing budget, Sobha has fallen more (>45%) than peers.")

Sobha’s stock price has tumbled by more than 45% since January 2020 beaten down by concerns around weak sales, rising leverage and promoter pledge. We now believe the stock has corrected excessively to an attractive level, particularly considering the imminent improvement in the company’s operating performance. Our analysis reveals niggling cash flow issues are cyclical—not structural—and that a reversion to mean should aid debt reduction. While we are increasing the discount to NAV from 10% to 25% and moderating NAV projections on the back of a general risk-off in the market and concerns around policy support for the realty sector, we maintain Buy with an SoTP-based revised TP of Rs 428 (Rs 645 earlier).

Multiple concerns underlie recent stock correction…

While most realty stocks have corrected heavily since January 2020 (BSE Realty Index down ~25%) in the wake of a disappointing budget, Sobha has fallen more (>45%) than peers. We ascribe this to: (i) flat sales trajectory, evident from 9MFY20 booking value; (ii) rising leverage (net debt up Rs 6.6 bn since end-FY19); and (iii) promoter share pledge (10.5% of overall shares pledged).

…but performance poised to improve

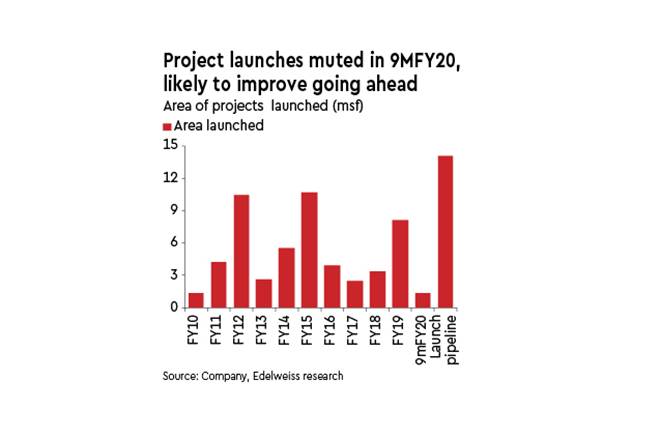

We believe these concerns are likely to be addressed sooner rather than later with sales and cash flows likely to improve—the launch pipeline stands at a robust ~14msf for the next five–six quarters (compared with ~1.4msf in 9MFY20). Cash flow deterioration is also due to temporary cyclical factors such as: (i) weak mobilisation advances in contracting business; (ii) stage of construction; and (iii) customer advances in the realty segment.

All these factors would revert to mean going ahead, which should drive debt reduction. Lastly, promoter pledge has remained largely constant over the last decade despite sizeable stock price movement, which indicates there is no material correlation between the two variables.

Outlook: Attractive

RERA-driven consolidation and the ongoing liquidity crisis are throwing up growth opportunities for organised players such as Sobha. Sales and debt trajectories remain the key variables for the stock though. Retain Buy.