Slower OEM auto sales may weigh on loan growth. Part of this is transient and could recover if visibility on rural capex improves post-election. Market-share gains and a rising presence in non-M&M products may cushion growth. Funding costs have edged up, but pricing power in rural markets is strong. The asset quality improvement story looks intact, with collections steady despite auto headwinds. Visibility on a normal monsoon could be a positive trigger. Buy.

Auto headwinds could weigh on loan growth

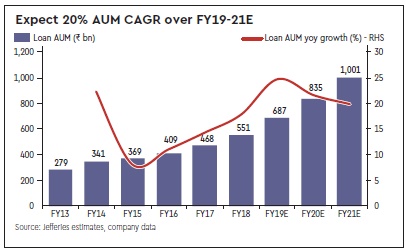

Auto data has been weak. Growth in rural areas (70% of AUM) has been better than in urban, but rural disbursal growth has also moderated in recent months. A cyclical slowdown in autos/tractors could weigh on loan growth, but: (i) market share gains and rising financing of non-M&M products; and (ii) strong growth in the pre-owned segment (less cyclical) should cushion AUM growth. Delays to new purchases amid uncertainty about the election outcome are also partly contributing to the slowdown which could prove transient. We cut our AUM estimates by 4% and forecast 20% AUM CAGR in FY19-21e.

Mapping past cycles

Our analysis of past cycles suggests loan disbursal growth at MMFS has broadly mirrored industry OEM sales/M&M sales. That said, correlation with OEM/M&M sales has fallen in recent quarters on an increase in financing of non-M&M products. The share of non M&M products has increased to 56% from 52% in FY17-19.

Funding costs to rise, but better pricing power, too

MCLR rate hikes (20 bps vs Q2, +50 bp vs March) could boost funding costs. Product mix changes and asset quality issues affected NIMs in the past cycle. Tractor mix would fall, likely offset by a higher mix of pre-owned vehicles. Stronger pricing power in rural markets should cushion the impact of higher funding costs.

Asset quality improvement story intact

Rural stress led by a poor monsoon was the key driver of a spike in GNPA/credit costs and fall in ROA in the past cycle. Rural collection is steady despite auto headwinds. Thus, asset quality improvement should continue. Monsoon uncertainty is a near-term overhang given El Nino risks.

Tweak estimates, maintain Buy

We lower FY19-20 EPS by 1-2% and target price to Rs 490 (Rs 500) as we trim our AUM estimates.