For Q1FY21, Kotak Bank reported profit of Rs 12.4 bn, down 9% y-o-y but above estimates with better fees and lower costs. Fall in moratorium loans from 26% last time to 9.7% is encouraging; bank accelerated NPL recognition & has contingent provisions of 0.6%. Management remains conservative on lending (loans down 2% y-o-y) and stays tentative on opportunity to grab share in loans despite scale-up of Casa to 57% of deposits. Clarity on CEO extension is key. Buy stays.

Encouraging decline in moratorium loans: Management clarified that 80% of moratorium loans are secured and hence even in case of slippages, the loss-given-default should be manageable. Key would be to see the normalisation of collections from loans that exited Phase 1 moratorium. Bank has accelerated downgrade of some stressed cases to NPLs which lifted NPLs by 12% q-o-q to 2.7% of loans. NPL coverage is at 68%.

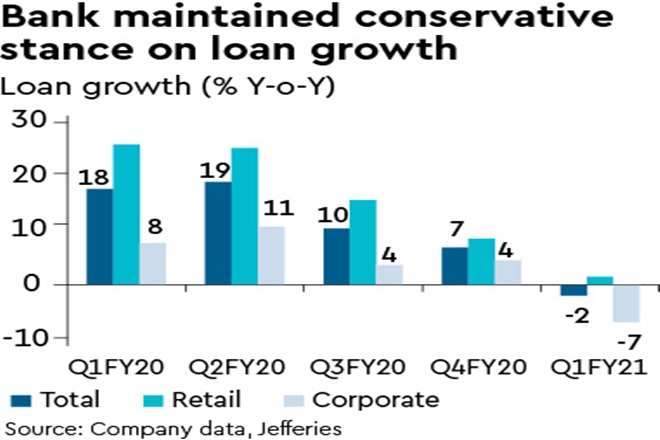

Holding tight on new lending despite stronger Casa: Management has maintained conservative stance on loan growth given the uncertainties; not only is the current trend weak with a 2% y-o-y decline (vs. sector growth of 6%), but it may stay weaker in near-medium term. On the Casa side, scale-up has been strong with 26% y-o-y growth to 57% of deposits, and with recent cuts to savings deposit rates, we see some upsides to margins that will aid NII growth (down 22 bps q-o-q in Q1).

As highlighted earlier, bank hasn’t fully leveraged improvement in deposit franchise/lower funding-cost to gain share in high quality corporate lending. Fees were down 33% y-o-y, still better than expected, and opex was down 10% y-o-y; unlike peers, Kotak Bank didn’t book treasury gains. Consolidated profit of Rs 18.5 bn was down 4% y-o-y and 49% higher than standalone profit.

Buy stays: We see weaker earnings growth in FY21 reflecting higher credit costs and weaker topline, but overall asset quality should hold up given conservative approach to lending. We maintain Buy with SOTP-based TP of Rs 1,570, including value of bank at 3.6x Jun-22 adjusted PB.