We hosted a Group Call with Nilesh Jetpriya – President, Morbi Ceramic Association. He cited that Morbi exports have sharply risen to 40-45% of production now, and could rise to 60% over long term. FY22 volume growth at 15-20% appears plausible. Morbi players could hike prices by +15%, due to cost inflation. This could alleviate competitive intensity and sustain pricing stability in domestic tiles market – KJC is the market leader. We raise FY22-24e EPS by ~3%. Retain Buy; PT at Rs 1,355.

Exports: Morbi cluster is the key supplier to exports. Exports appear to be de-risking geographically, with GCC now at 25% of exports (earlier 45%), followed by the USA at 10-12%. Overall tile exports could rise to ~60% of Morbi production over the longer term. KJC is domestic-focused, with negligible exports.

Rising input costs; price hikes: With a view to pass-on input cost escalation, Morbi players could hike prices by +15% going forward. This augurs well for organised players, as their price differential converges with the unorganised players.

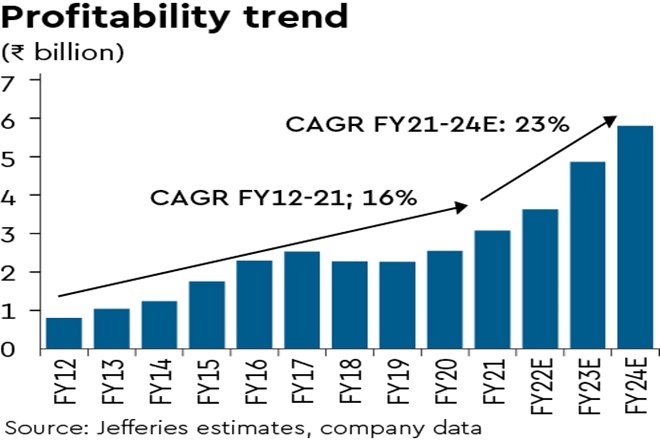

Positive read-through for KJC: KJC is likely to benefit from rising Morbi exports and price hikes. We raise KJC’s FY22-24e EPS by ~3%, in view of sturdy catalysts – (i) Housing revival; (ii) market leadership; (iii) optimising mix (60% value-added sales); (iv) market share gains (export focus by Morbi players); (v) margin focus (retained 15%+ over FY16-21); and (vi) B/S strength (net cash).

We view KJC as a robust play on housing revival / home furnishing. Retain Buy with revised PT of Rs 1,355 (vs Rs 1,250). Retain target PE at ~40x, a premium to hist. 5-yr avg. KJC stays one of our Top SMID Picks.