Strong domestic steel prices should sustain near term, driving higher margins in Q4, but we see this as an opportunity to take profits as domestic prices should soften post Q4 as (i) spreads may ease as Chinese supply ramps up post winter cuts; (ii) seasonal factors and dom. supply outages fade. Q4 results should be strong, but stocks have usually peaked ahead of margins. Retain UPF on Tata, SAIL, JSW. Prefer HNDL for leverage to metals/global macro recovery.

Winter restrictions nearing an end; Can spreads sustain?

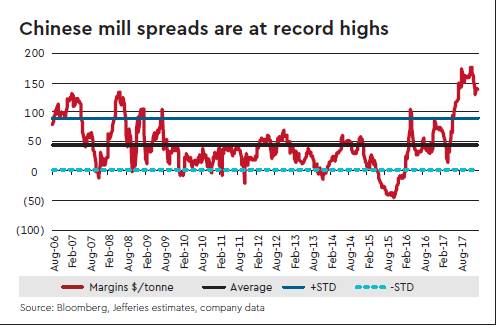

Capacity closures, strong Chinese steel demand have lifted Chinese mill utilisation to over 80% in CY17 (75% CY16). Winter restrictions till mid March have pushed effective utilisation further to over 90%, supporting the record high spreads that we see currently. Seasonal pick-up in Chinese demand post Chinese New Year along with ongoing winter restrictions should support strong spreads and regional steel prices near term, but steady ramp-up of output (down 80 mn tons vs. Aug annualised) and slowing Chinese demand may lead spreads to moderate, especially as effective utilisation falls back to mid-80s. Spreads at Chinese mills are $138/ton vs. 10 year average $45/ton (average +SD $86/ton). Moderation of spreads to even high, but more sustainable levels may weigh on regional prices.

Restraints beyond winter heating season could be supportive

China’s Handan city (annual output 52 mn tons) has extended 50% BF capacity restriction till end of March (mid March). This could impact steel output by 2 mn tons. There are talks that Tangshan may restrict blast furnace output by 10-15% based on weather conditions over March- Nov (potential output impact 9-10 mn tons). Henan local government, on the other hand, is planning 30% output restriction over the next heating season (vs. 50% this year). We believe winter restrictions should recur, but mills/supply chain would likely be better prepared.

Domestic steel prices firm near-term

Domestic HRC prices are up Rs 3,000/ton YTD and rebar prices are up Rs 3,500/ton YTD CY18. While Q4 is seasonally strong, other factors that have supported strong prices include (i) good demand (+6.8% y-o-y Jan) and restocking; (ii) strong regional prices; (iii) input cost push and (iv) tighter domestic supply due to unplanned outages at Tata, SAIL and strong export bookings in December quarter. Q3 rebar export runrate (annualised) was around 10% of domestic rebar demand.

But prices should soften post 4Q

Mills are reportedly planning another Rs 1,000-1,500/ ton price hike in March, but there is uncertainty around whether this sticks. Domestic steel prices are at 3% discount to FTA based import parity (8% discount to Chinese import parity) which gives some headroom, but with initial restocking now over, buyers have started to resist price hikes. Exports have declined as domestic sales are more profitable (net exports -30% m-o-m in Jan). Supply disruption led tightness should ease. Potential pullback in regional steel prices post Q4 should weigh on domestic prices.

Elevated spreads = strong Q4; but opportunity to take profits

Q4 margins should be strong given higher domestic steel prices. Spot HRC spreads at non-integrated mills are up Rs 1,260/ ton q-o-q (lagged spreads Rs 216/ton). Strong Q4 margins are well anticipated. We believe markets would focus on outlook for spreads/margins beyond Q4.

Risk reward appear negative

Steel fundamentals have improved, but we have doubts around sustainability of current high spreads. Domestic steel prices are at multi year highs and are likely near a peak. Potential pullback in spreads/ regional prices may drag domestic steel prices lower. Indian steel stocks are trading at 7.2-10.5x FY19e Ebitda at a premium to historic average (6-6.5x). We think stocks are already extrapolating Q3/Q4 margins to sustain. Key risk to our view are (i) more Chinese supply reform measures, output restraints outside winter heating period; (ii) tighter than expected world ex China markets.

Spreads unsustainable, but collapse unlikely

As part of supply side reforms, China has closed around 137 mn tons of illegal Medium Frequency Furnace capacities. It also curtailed around 50 mn tons of capacity in CY17. This has effectively lifted utilisation levels in China to around 81% in CY17 from around 75% levels in CY16. Production restriction during winter heating season has affected production further. Construction activity picks post Chinese New Year, while ongoing winter restrictions in March imply supply will likely remain constrained. This could lead to short term tightness in Chinese markets, supporting higher steel prices/spreads. That said, trader inventories for rebar have increased 1.4x CY18 (-8%YoY) and for flat products have increased 25% YTD CY18 (flat on a y-o-y) basis. This could be a buffer.