Over the past month, NIFTY has rallied 8% and recovered 65% of its YTD underperformance vs. the region (MXAPJ). The rally has been broad-based and led by cyclical sectors, mid/small-caps and value stocks. Foreign inflows have notably picked up with FII net buying $4.5 bn in the past one month as market expectations of a potentially stable government have risen in recent weeks.

Election playbook: Cyclical rally; rotation out of ‘quality’ to ‘value’

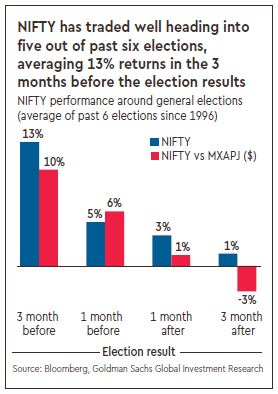

NIFTY has rallied in five out of the past six general elections since 1996 with average 13/5% returns in 3-mo/1-mo before the election results. Cyclicals like banks, industrials, materials and autos have led. Stylistically, investors have rotated out of ‘quality’ stocks (strong balance sheets, stable growth) into value and mid-caps.

What’s priced? Valuations fair relative to fundamentals but likely ‘overshoot’ n/t

Current domestic macro and market set-up looks better on most metrics compared to 2014 rally but current starting point for valuations is higher. At 18x P/E, current P/E looks ‘fair’ relative to the macro backdrop, but we see potential for valuation overshoot in the near term. Combining our implied cost of equity models, relative P/E premium and earnings/bond yield gap analysis, we estimate an average 10% P/E ‘overshoot’ if valuation metrics go to the extremes seen during 2014/15.

Our View: Raising India back to overweight; NIFTY 12500 target in 12 months

We lowered India to marketweight in September on n/t macro/earnings risks, rich valuations and political risks. We raise it back to OW given sharp underperformance in January/February, better Q3 earnings and a pick-up in FII positioning from lows amid rising market expectations of a potentially stable government. We expect earnings to grow 16% this year (highest in the region) and 18x target P/E with NIFTY to reach 12,500 in 12 months.

Upside Ideas: Value Cyclicals, Oversold quality Mid-caps, NIFTY short-dated calls

Sectorally, we favour banks and domestic cyclicals over exporters and defensives. We recommend short-dated NIFTY calls, value cyclicals and oversold quality mid-caps to participate in the current rally.