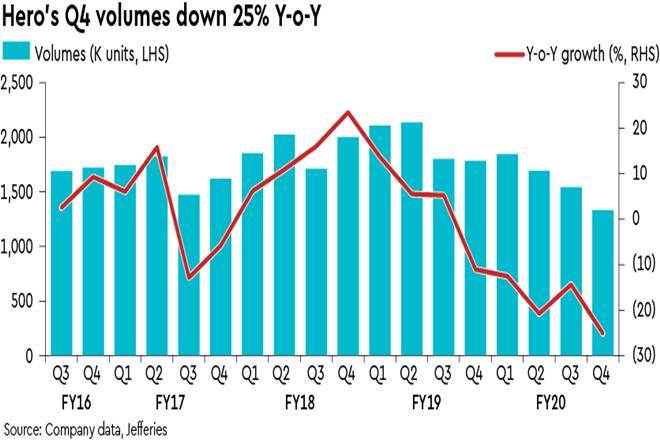

Hero’s Q4 volumes fell 25% y-o-y while Ebitda, adjusted for one-time items, was down 23% y-o-y (in line with our estimates). Hero said that demand outlook is uncertain amid Covid-19, but was optimistic on rural and personal mobility shift. We expect Hero’s volumes to decline for a second consecutive year in FY21, but then see a rebound in FY22-23 on two years of low base. Its 18x FY21e and 14x FY22 PE are reasonable to play the next 2W up-cycle. We retain Buy.

Weak Q4 results: Hero’s Q4 volumes declined 25% y-o-y, partly pulled down by the start of Covid-19 related lock-down in March. Q4 reported Ebitda was down 38% y-o-y but included: (i) one-time cost to clear BS4 dealer inventories; and (ii) provision related to the uncertainty of fiscal benefit at one of the plants. Adjusted for these two items, Q4 Ebitda was down 23% y-o-y (in line) and Ebitda margin was down 70bp y-o-y to 12.9%. Q4 reported net profit at Rs 6.2 bn was down 15% y-o-y. In FY20, Hero’s volumes and Ebitda fell 16-18% y-o-y, while recurring net profit declined 4% y-o-y.

Demand uncertain but improving: Hero said that demand outlook is uncertain amid Covid-19 but inquiries, as well as conversions, are picking up. Hero was optimistic on the rural economy, pent-up demand coming back and personal mobility shift. All of Hero’s plants and suppliers have re-started, although utilisation levels are low. About 90% of dealers have commenced operations too. Hero has also intensified internal cost-cutting efforts and is targeting 100bp reduction in FY21 (FY20: 50bp).

Capital spend plan for FY21 has also been cut from Rs 10 bn to Rs 6 bn. Hero had dealer inventories of 550K at start of FY21, which appear high in the current demand environment (FY20 average monthly wholesales was 519K). About 43% of Hero’s sales were financed in FY20, of which 46% was from Hero Fincorp; Hero invested an additional Rs 2.5 bn in Hero Fincorp in Q4.

FY21 outlook weak but FY22-23 should be better: We expect FY21 to be the second consecutive year of volume decline for Hero as the economic impact of Covid-19 and BS6 cost increases will keep demand weak. Entry-level motorcycles are also facing higher percentage price increases for the BS6 norms; however, a better rural outlook and potential down-trading amid Covid-19 should provide a cushion. We expect FY22-23 to be good years for Hero as Indian 2W demand rebounds on two years of low base. We factor in Hero’s volume falling 11% in FY21, followed by 10%/7% growth in FY22/FY23. It is launching a new 160cc motorcycle (Xtreme) with shipments starting in Q1, and any success here could improve the long-term outlook.

Valuations reasonable to play 2W demand recovery: We find valuations at 18x/14x FY21e/FY22e PE and 3.0x FY21e PB (for 20% ROE in FY22-23) reasonable to play the Indian 2W demand recovery. Hero has a strong balance sheet with Rs 65 bn of cash at end-FY20 and FCF yield of 4-5% in FY21-23e. We fine-tune estimates and retain Buy. Our PT of Rs 2,725 is based on 17x FY22e PE (slightly above the last ten-year average of 16x). Key risk is an elongated demand downturn in Indian 2Ws.