It was a modest quarter for HDFCB: (i) Retail loans saw moderation (high base, 2w/auto slowdown), spurt in wholesale (short-term opportunistic), (ii) elevated provisions – building contingent provision for expected Agri NPLs in Q1, and (iii) slower core fee growth. NIM at 4.4% & core-PPOP/Assets of 4.6% (highest since FY15) were better. Post election rhetoric and implication on Agri to be key driver going forward. We pencil in risks and cut EPS. Retain Buy, price target of Rs 2,685.

Non-retail loan growth spurt

Overall loans grew 24.5% y-o-y, retail at 19.0% y-o-y and wholesale 31.2% y-o-y, the latter an outcome of short-term opportunities and NCLT consolidation. Retail loans moderated on the back of higher base in personal & business loans and slowdown in 2w/auto sales. Much of this is normalisation of post demonetisation spurt. Overall deposits grew 17% y-o-y, with time-deposits at 19.4% y-o-y, while savings were softer at 11.1% y-o-y, though management maintained its customer acquisition in deposits remains robust with a conscious strategy of growing time-deposits through higher deposit rates.

Fee moderates to ~11% y-o-y

The weakness was driven by (i) high base and normalisation of demonetisation’s positive impact on payments/cards,

(ii) regulatory change to mutual fund distribution fees on trail fee model, and

(iii) lower processing fee owing to weak disbursal, especially in 2w/auto segment. We think the trends should steady from Q3 onwards but at lower levels than last two years.

Also read: Uber may not reach $100 billion valuation with target share price of $44-$50 for IPO

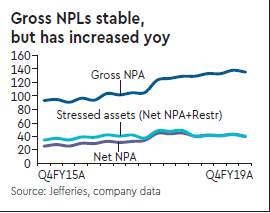

Asset quality stable, Agri NPLs are key

Gross NPLs were largely stable at 1.36% (vs 1.38% in Q3FY19 and 1.3% a year ago). The slippage ratio for the quarter was 2.2% (based on 12m trailing loan book), versus 2.5% for Q3FY19 and 2.0% for Q4FY18. Agri slippage is seasonally higher in Q1/Q3 quarters and to that extent, the bank has created contingent provisions. Management hopes that with national elections behind us, further risks to Agri NPLs should be lower, but it remains key to asset quality. We are, however, a little less sanguine.

Stable NIM, PPoP/RWA strong

NII growth was 22.8% (3.0% above JEFe), NIMs were at 4.4% (v/s JEFe 4.37%). Expenses grew 17.6% y-o-y, which helped core PPoP to grow at 19.8%. Core PPoP/RWA at 4.6% was the highest since FY15.

Estimates change

The next two quarters could be weaker for which the bank may have to swing growth toward retail and utilise the accumulated provisions to manage bottom line growth. Our EPS estimates are lower by 7% factoring in moderation in fee income and higher provisions. We largely maintain NIM & loan growth estimates. Forecast FY19-21e EPS CAGR of 23.3% and adj. BVPS CAGR of 15.7%.

Valuation and historical multiples

HDFCB currently trades at 4.1x book (Mar’20) and 23.9x EPS (12m to Mar’20e). At a PT of `2,685, the implied multiples are 4.1x book (Mar’21e) and 22.7x EPS (12m to Mar’21e). This compares to 5-year averages of 4.11x and 20.6x, respectively.

Downside Risks: Weak Core PPOP trend, asset quality inches up on retail.