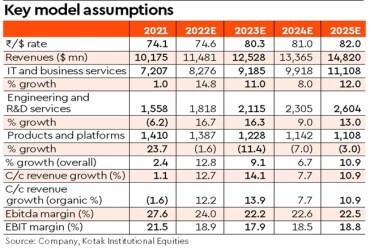

The key highlights from HCLT’s analyst meet are the impact of macro on demand, drop in discretionary spending in hitech, telecom and a few other verticals, and furloughs has been higher than expected. The company now expects revenue growth for FY2023 estimates to be at the lower end of its guidance band. The bookings trend will likely be robust for the December 2022 quarter and reasonably healthy in 2HFY23. Maintain Buy rating with an unchanged FV of Rs 1,250. HCLT had guided for revenue growth of 13.5-14.5% in c/c for FY2023 estimates.

HCLT expects an increase in vendor consolidation trends due to a few factors— (i) clients wish to narrow down the vendor list to strategic partners who can scale up digital transformation, (ii) quite a few large vendors are on a weak footing and (iii) share gains from smaller firms and boutiques as clients scale digital transformation throughout the enterprise. The company is confident of emerging as a beneficiary from the trend. The services portfolio is closer to clients’ spending patterns compared to the heavy dependence on IMS and ER&D in the past. The applications portfolio will continue to strengthen. The digital business, including consulting, modern apps and data/analytics, drove 50% of incremental growth in FY2022. The company will continue focus on accounts with large tech spends which aided growth in FY2022— 85% of growth from 50 accounts.

Also Read: Max Healthcare Rating: Buy | Continues to deliver stellar performance

The strength in applications, higher ER&D mix and leadership in IMS will lead to a more consistent industry-matching growth profile in the medium term. The large deal engine is firing well with more opportunities, given the rising trend in vendor consolidation and costefficiency focused deals.