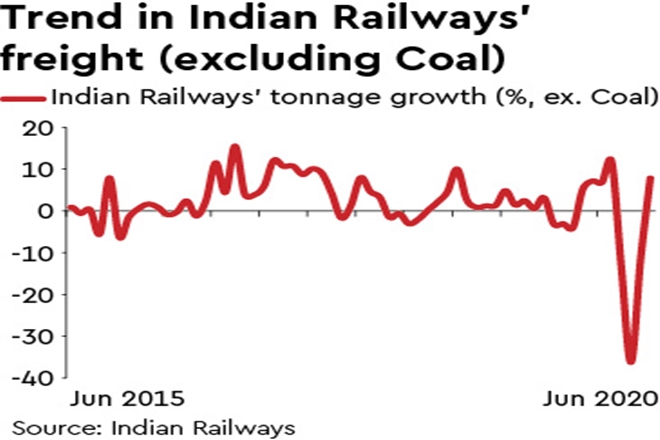

In its quarterly volume update, CCRI reported that its FY21 Q1 total handling volume fell 21% y-o-y to 0.73 million. CCRI’s 20% Export-Import (EXIM) volume decline compares favourably with India Major Ports’ container volume decline (down 30% in Q1). CCRI’s better than port container volume performance is driven by a higher share of rail mode of transportation, which could have been partly offset by CCRI’s loss of market share in the rail industry.

Rail market share has been higher in recent quarters due to greater COVID led disruptions in road transport. However this trend is temporary and we see it reversing from Q2FY21 until the Dedicated Freight Corridor (DFC) gets at least partially commissioned (FY21 Q4).

Upside risk to guidance: During the last earnings conference call, management had guided for 20% decline in FY21 volume. Following Q1 update, with a recovery in freight volumes and benign base for rest of the three quarters of FY21, we now expect CCRI’s volume to fall by ~11-12% during FY21e vs. our 17% decline forecast earlier.

FY21 Q1 preview: For revenue driver originating volume, we expect a higher 27% y-o-y decline compared to a 21% fall reported in handling volume. This, coupled with lower lead distance as well as inferior business mix, drives our 31% drop in revenue forecast. We expect Rail freight margin to improve y-o-y; though it would be more than offset by higher land licence fees and fixed overheads, resulting in 710bps y-o-y decline in Ebitda margin. We expect Ebitda/post-tax profit to decline by 51%/63%.

Investment summary: In earlier notes, we had argued that the current share price appears to underappreciate the prospect of dominant player CCRI (66% market share in FY20) being privatised as the industry’s growth outlook is set to improve from the partial commissioning of the Western DFC (FY22e) as well as the exploratory growth opportunities.

Retain Buy rating: While we have increased our FY21e estimates by 8% driven by higher volume forecasts, our FY22e/23e expectations are broadly similar, resulting in an unchanged TP of Rs 500. The shares are trading at 28x FY22e, while our TP implies 32x. Downside risks: The government could call off its planned disinvestment and railway haulage rate increases.