Dedicated Freight Corridor (DFC), last mile connectivity and working on new growth opportunities were highlighted in Concor’s AR. Government ownership limited the FY21 fixed cost cuts unlike private companies. This gives comfort on our volume recovery based FY22e 335 bps y-o-y margin rise. We raise our PT by 2% factoring in the FY21 AR and believe re-rating triggers of volume growth and operating leverage are intact. Privatisation is the additional upside. BUY.

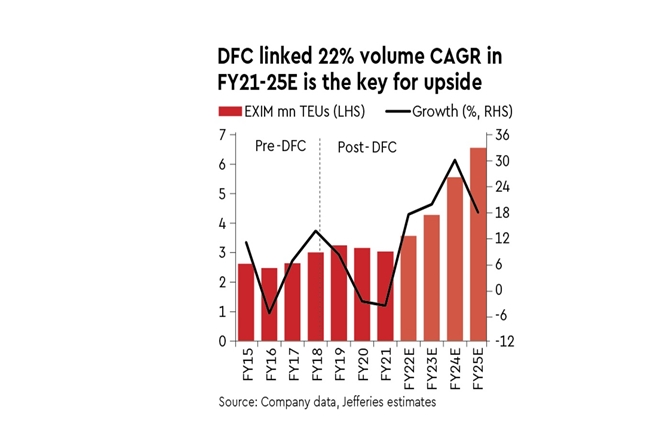

Management strategy focused, even with privatisation plans: FY21 saw reorganisation to a leaner 2-tier structure of Corporate Office and Terminals and area divided into 4 regions vs multiple earlier. Faster and decentralised decision making was the aim. Additionally, last Mile connectivity was an edge private sector had, which Concor has also developed. Owned/leased number of containers rose by 22% YoY in line with the 20%+ y-o-y growth trajectory that began in FY19 in anticipation of DFC commissioning.

Multiple triggers in H2FY22E: Delhi-Gujarat ports connectivity should be completed end FY22e, post which volumes should see a steep jump in growth. Management on its Q1 call mentioned LLF outflow could be Rs 3.75 bn vs Rs 4.5 bn and could add 5% to our FY22e EPS. Q1 call also discussed Rs 60-70 bn outflow on 35-year land lease vs our Rs 75 bn assumption, which could add 4% to our FY23e EPS. Disinvestment is an additional upside, that should play out over the next 12-18 months. Our revised Rs 870 PT (vs Rs 850) values the company at 20.5x EV/Ebitda FY23e – in line with the 7-year average and mirrors our DCF value.