Coal India reported 366% yoy growth in net income to Rs 60.3 bn for 4QFY19, closing full-year FY2019 at a net income of Rs 175 bn (+149%yoy). Earnings growth should be seen in context of a favourable base due to non-recurring employee cost in the base quarter, though boosted by 8.5% yoy growth in blended realisations in FY2019 including 43% yoy growth in e-auction realisations. Maintain Buy with unchanged fair value of Rs 290/share.

Headline growth boosted by higher wage provisions in base quarter, sales

CIL reported net income of Rs 60.3 bn (+366% yoy) compared to our own estimates of Rs 47 bn. Headline growth was aided by non-recurring wage cost of Rs 74 bn in 4QFY18, as well as additional wage-linked provision of Rs 15 bn for full-year FY2018. Headline PAT growth notwithstanding, CIL reported revenue growth of 6% yoy on account of modest growth in volumes (+2.9% yoy) as well as realisations. Higher-than-estimated revenues were on account of continued improvement in blended realisations to Rs 1,603/ ton in 4QFY19. E-auction realisations remained robust reporting an increase of 30% yoy to Rs 2,754/ per ton; however, a 43% yoy decline in e-auction volumes led to a 25% yoy decline in e-auction revenues for 4QFY19.

FY19 performance

CIL ended full-year FY2019 with revenues of Rs 929 bn (+14% yoy), EBITDA of Rs 183 bn (+239% yoy) and PAT of

Rs 175 bn (+149% yoy). We view the performance of FY2019 as a reversion to normalised earnings, as the reported PAT for the preceding two years was impacted by non-recurring wage provisions, revision in employee cost, and a back-ended price increase (taken in January, 2018).

Maintain BUY rating

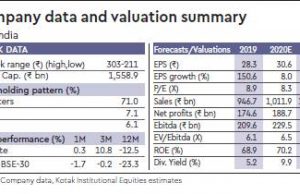

Coal India has had a much improved year with FY2019 delivering 149% yoy growth in earnings on the back of

14% yoy growth in revenue. The continued divestment by the government has made for valuations to be incrementally attractive at 7X P/E and 5.2X EV/EBITDA on adjusted earnings coupled with 10% dividend yield on FY2020E earnings. We have revised our earnings for FY2020E/2021E by 11% to factor in lower production cost. Maintain Buy with unchanged fair value of Rs 290.