APNT’s sales (up 11.9% y-o-y), Ebitda (down 2% y-o-y) and PAT (1.6% y-o-y) came below our estimates. Softness was largely led by gross margin pressure, higher ad spends and new plant ramp-up costs while double-digit volumes growth was a positive in our view given soft macroeconomic environment. Despite earnings volatility, we remain positive and maintain Buy given superior topline profile and scope for margin expansion as new plants ramp up.

Decorative business: Decorative business saw 10% y-o-y volume growth in Q4FY19 on a base of 10% y-o-y. This was the fifth consecutive quarter of double-digit volume growth which in our view is also led by market share gains from the unorganised players. Standalone business saw top-line growth of 12.2% y-o-y in Q4FY19.

International and industrials: Growth in these segments was softer due to slowdown in the auto OEM segment (PPG-AP) and macro-economic pressures in international geographies. Industrial JV however did well for the company.

Also read: Stock corner: Buy Larsen & Toubro, performance in the quarter was a mixed bag

Margins: Consol. and standalone gross margins were down 168bps y-o-y and 165bps y-o-y. Consol and standalone Ebitda margin were down 233bps y-o-y and 262bps y-o-y, respectively.

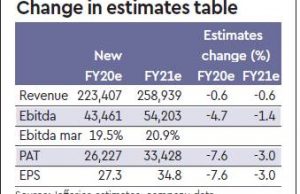

Outlook: Given FY19 EPS miss of 6% due to lower margins, we cut FY20 EPS by 7% but FY21 only by 3% as operating leverage of new plant ramp-up will kick in fully in FY21. We remain positive on the overall top-line growth trajectory of the company supported by strong execution and market share gains. Though margins have come under pressure due to higher RMs and new plant, we believe that it is now behind us and the company has a high visibility of strong double-digit earnings growth. We maintain our target multiple of 45x FY21 EPS to arrive at PT of Rs 1,575.