Infratel reported muted but better than expected quarter with revenues 4% and margins 90bps ahead of expectation. The beat though was entirely led by higher energy cost and margin. Tenancies saw further exits with FY18 seeing exits for c10% of overall tenancies. We expect near term earnings to remain muted as Voda/Idea exits are still ahead. With stock trading at 9x FY20 EV/Ebitda, and our concerns on long term margins, we maintain our Hold.

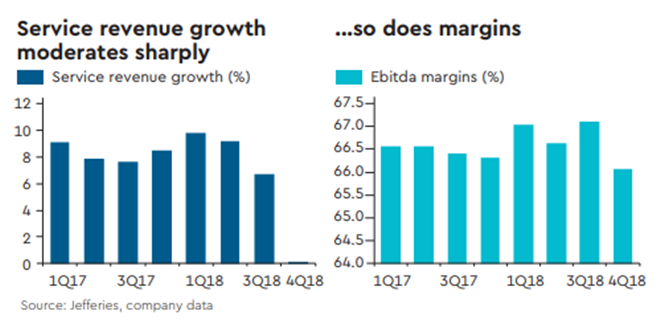

Muted results: Infratel reported muted quarter though slightly better than expectation. Revenues grew 4% y-o-y (JEFe 4%) and margins declined 117bps y-o-y (JEFe 200bps). The beat was led by energy revenues. Energy revenues grew +10% y-o-y while service revenues were flat. Energy Ebitda increased 18% y-o-y while service margins declined 30bps y-o-y.

Tenancies see c10K exits: Q4 saw 9813 tenancy exits. Of this standalone saw 3956 exits and Indus the rest. Overall FY18 has seen 22,134 exits (10% of total tenancies). Of these 2,514 exits have not yet happened. Interestingly, tower addition improved in the quarter to 444 towers vs 52 in Q3.

Near term earnings growth muted: We expect near term earnings for Infratel to be flat as operator consolidation impact offsets 4G rollouts. The Idea/Voda merger impact is ahead of us and mgmt indicated that it could be c20K tenancies for the company. We expect Ebitda to grow at 1% CAGR over FY18-20e, led by 2.6% revenue CAGR and 170bps margin decline. We expect dividend yield to remain high at 3.5%.

Long-term dynamics: While in the near term, earnings and return ratios are largely shielded, we are cautious on long-term outlook. With operators likely to remain under pressure, there may be stress on growth and margins for tower companies too. While Infratel makes c20% RoCEs, operators are expected to be below that even over medium term. We expect margins to see gradual moderation as increments and loading charges are negotiated.

Valuation/risks

We marginally tweak our estimates and our FY19-20 EPS change by c1%. While Infratel islargely shielded from the turbulence facing operators in the near term, we are concerned on medium term margins. Trading at 9x FY20 EV/Ebitda, we believe the stock is fully valued.We maintain Hold and price target of Rs 300.