Americans born in 1960 will turn 65 in 2025, but they will be eligible for Social Security’s full retirement age (FRA) until they are 67. This is the most recent milestone of a two-year progressive increase from the customary age of 65 to 67, which began in 1983, reports Newsweek.

In 2025, Social Security’s full retirement age will change once more, continuing a trend that impacts millions of Americans who are getting close to retirement. The official age of eligibility for full Social Security retirement benefits for individuals born in 1960 is now 67.

The increase in the full retirement age (FRA) is the result of a progressive shift that began with the Social Security Act modifications in 1983, which were designed to account for greater life expectancy and financial stability concerns within the program.

The FRA is the age at which seniors are entitled to receive Social Security retirement benefits without incurring a financial penalty for retiring early.

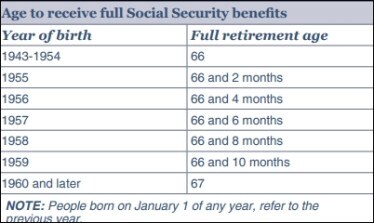

Full Retirement Age

If you were born in 1958 or earlier, you’re already eligible for your full Social Security benefit. The full retirement

age is 66 if you were born from 1943 to 1954. The full retirement age increases gradually if you were born from 1955 to 1960 until it reaches 67. For anyone born 1960 or later, full retirement benefits are payable at age 67.

Early or Delayed Benefits

Americans can still claim Social Security as early as age 62, but there is a cost to it. Early claimants receive a lower monthly benefit, roughly 30% less than they would have at 65, now 67.

You can start receiving your Social Security retirement benefits as early as age 62. If you start receiving benefits early, your benefits will be reduced by a small percentage for each month before your full retirement age. However, you are entitled to full benefits only when you reach your full retirement age. If you delay taking your benefits from your full retirement age up to age 70, your benefit amount will increase.

Social Security Administration’s latest guidance outlines these differences: someone eligible for a $1,000 monthly benefit at age 67 would receive only $700 a month if they claim at 62.

If they waited until age 70 increases that monthly amount to $1,240—a 24-percent boost for delaying three years past the FRA.

When to Claim Full Benefits

Those born after 1960, who will turn 65 in 2025, must wait until 2027 to get their full retirement benefits at age 67, while those born before 1960 can claim their full benefit in 2025.

The chart below lists the full retirement age by year of birth

For most Americans, this new rule is likely to make their life tough. Nearly 4 million Americans are expected to reach the age of 65 by 2025.

Social Security actuaries predict a retirement benefits shortfall, with the trust fund potentially depleted by 2033, limiting the system’s ability to cover 77% of scheduled benefits, according to a 2024 report.

Deciding the Age For Benefits

Deciding when to begin receiving retirement benefits is a crucial decision. Social Security benefits replace a portion of a worker’s pre-retirement earnings.

The amount of your average wages that Social Security retirement benefits replace varies depending on your earnings and the date you choose to begin payments.

If you start receiving benefits at age 67, the percentage goes from 78% for extremely low earners to roughly 42% for middle earners and about 28% for high earners.

If you start receiving benefits before the age of 67, these percentages will be smaller. After age 67, they would be higher.

Most financial planners suggest that you will need around 80% of your pre-retirement income to live comfortably in retirement, which includes Social Security benefits, investments, US stock market holdings, and other personal savings.