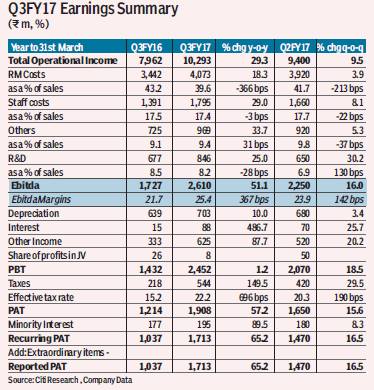

The third quarter was an encouraging one, not just in terms of financials but also several positive trends in the business viz. good progress on global biosimilars initiatives and strong traction in small molecules. Results beat expectations as well, with strong growth across the board (Revenues/ Ebitda/PAT up 29%/51%/65% y-o-y), respectively on a smart pick-up in biologics, small molecules and licensing income.

Key to note: (a) Malaysia facility commercialised, a three-year Rh-insulin contract worth c Rs 4.6 bn from the Malaysian govt. to help grow EM biologics sales c3x over the next two years; (b) Received TAD in Sept 2017 for Trastuzumab biosimilar from the US FDA; (c) Bevacizumab moving into global Ph-III trials; (c) Rosuvastatin API sales drives healthy growth in small molecules; (d) R&D at 12-14% of Biopharma in FY18; (e) Copaxone: some queries pending, approval unlikely in near term.

Progress on biosimilars continues: (a) Received a TAD for biosimilar Trastuzumab for Sept 2017; (b) Filed for Insulin Glargine in EU; (b) Bevacizumab enters global Ph-III trials; (c) Malaysia facility for insulins commissioned; (d) Expects to grow EM biologics sales 3x over the next two years.

Implications: We slightly tweak estimates (FY17e/FY18e EPS: +3.9%/-0.2%) and revise TP to Rs 1,180/sh. Biocon remains India’s most leveraged play on the global biosimilars opportunity and we now see tangible progress in its efforts to target the same. The stock has had a very good move but we believe it still remains largely under the radar for a large set of investors as a biosimilars play. We expect the tangible progress made on this front to support premium valuations. Our new TP includes a value of Rs 425/sh (vs Rs 415/sh earlier, tweaking Rupee/Dollar estimate) for the company’s lead biosimilar molecules and Rs 755/sh. Maintain Buy.

Valuation: We set a target price of Rs 1,180 for Biocon which is a sum of two parts. We assign a probability adjusted NPV of Rs 425 to its lead biosimilar products. We assume 75% probability of launch for trastuzumab, pegfilgrastim and glargine, 60% for adalimumab and 50% for bevacizumab—guided by progress/ milestones on each. We value rest of the business (small molecule APIs, branded formulations, research services etc.) at Rs 755 (20x March’18e EPS). This is at a c15% discount to our target PE multiple for its mid-cap peers such as Glenmark and Cadila. Since pharma is a growth sector, we prefer to use P/E v/s EPS CAGR as our primary valuation methodology for base business of pharma companies.