The Reserve Bank of India’s (RBI) recent move to permit domestic lenders to finance acquisitions may open the door for them in sectors such as pharmaceuticals & healthcare, energy, infrastructure, industrials and renewables, said top investment banking sources. These segments have seen consolidation in the last few years, data from EY show, with as many as three big M&A deals valued at $1-3 billion reported in these verticals in the first half of this calendar year.

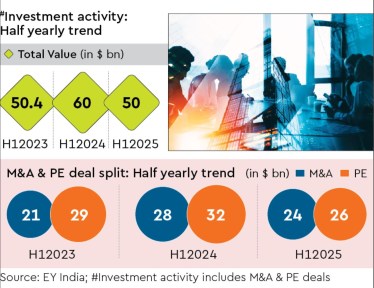

India Inc’s total investment activity in the first half of this year touched $50 billion across M&A and PE deals, 16% below the same period last year, but in line with the trend seen in H12023, when total investment activity stood at $50.4 billion, according to EY data. M&A and PE deals in H12025 were nearly evenly split at $24 billion and $26 billion each. The previous two years show a sharper tilt towards PE deals. (See chart)

Experts say that sectors such as pharma, energy and infra give banks the opportunity to get “hard collateral” (such as land, buildings and plants) against loans versus “soft collateral” or shares. Banks can also fund up to 70% of the acquisition value, with 30% coming from the acquirer’s own equity.

Sources in the know said that banks are likely to come up with their internal frameworks for acquisition financing in the next few months in line with the guidelines prescribed by the central bank. These include capping bank exposure to 10% of its Tier 1 capital, funding transactions involving listed acquirer entities and a debt-equity ratio of 3:1 post acquisition, which will come into force in April 2026.

While some experts argue that the rules are too “prescriptive”, others such as Deep Mukherjee, partner at BCG, are of the view that a prefixed debt-equity ratio may require reconsideration.

Typically, infrastructure deals see debt-equity ratios touching 4:1, said experts, implying that banks may have to rewire their thinking there. “The real value lies in synergy, understanding how two businesses, their cultures, and operations will integrate to unlock future cash flows. That demands advanced analytics, simulation capabilities, and deep sectoral insight,” Mukherjee said.

Sanjay Dutt, MD & CEO, Tata Realty & Infrastructure, said the inclusion of domestic banks will reduce cost of capital for firms. “Bank debt is cheaper than other forms of finance. We see no concerns as finance costs will come down,” he said.

An executive director at an infrastructure firm said while foreign credit funds and alternate investment platforms provide debt at about 18-24% in terms of interest rate, domestic banks could land up lending at a lower 14-15% interest rate to attract business. “If that happens, it will be a win-win for both the corporate house and the domestic lender, providing the latter a new avenue to lend,” the executive said, declining to be quoted.

Manish Aggarwal, partner, Deloitte India, said domestic banks could land up cornering up to 15-20% market share in acquisition financing within 12-18 months of the norms coming into force, if risk profiles are mapped out well, internal frameworks are robust and deal structuring skills are put in place quickly.

“Most domestic banks have existing relationships with top borrowers, which could be leveraged for acquisition financing. Typically, top borrowers have exposure to capital intensive sectors such as pharma, energy and infrastructure, where the need for acquisition financing has been growing, given the consolidation within these segments,” Aggarwal said.

Nitin Jain, partner, debt and special situations, strategy and transactions, EY India, said that while bigger banks may be quick to tap the market for acquisition financing, smaller and mid-sized public sector banks may take time to adapt to the change. “As a result, the effective and wide implementation of these guidelines could be somewhat delayed,” he said.

According to Capitaline, 32 public and private sector banks have a combined net worth of close to Rs 28 lakh crore, making nearly Rs 2.8 lakh crore available for acquisition financing.

Sanjay Agrawal, senior director at CareEdge Ratings, said banks are being positioned as “fixed-rate capital providers”, not bearers of “end-of-tail risk”. “That is a critical distinction,” he said. “The RBI wants to avoid scenarios where banks are left holding the bag if a deal goes south,” he added.