In a bid to further improve the cash position of banks, the Reserve Bank of India (RBI) on Thursday provided additional 2% liquidity window within the mandatory statutory liquidity ratio (SLR) requirement to the lenders by tweaking liquidity coverage ratio (LCR) norms.

The LCR indicates the proportion of highly liquid assets held by banks to ensure their ability to meet short-term obligations.

“We have allowed additional 2% of LCR to reckon as Level 1 high quality liquid assets for the purpose of computing the LCR of the banks. While this move will harmonise the liquidity requirements of banks with LCR, it will also release additional liquidity for lending by banks,” RBI governor Shaktikanta Das said after unveiling the first bimonthly monetary policy for 2019-20.

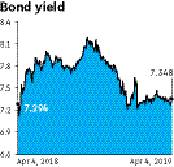

Yields on the benchmark bond maturing in 2028 rose by 9 basis points (bps) 7.506% — the highest single-day rise in the past two months. The rupee depreciated by 74 paise to close at 69.16 against the US dollar, its highest single-day fall in four months.

“RBI’s carve-out of liquidity coverage ratio (LCR) from the SLR by 2 percentage points of the net demand and time liabilities (NDTL) has lowered the need for banks to step up bond purchases to meet regulatory norms but is also a negative for the bond markets,” said Radhika Rao, economist at DBS Bank.

The pressure on the central bank to maintain a supportive role in the debt markets increases, similar to FY19, she observed.

“There would be no direct impact in the market in terms of liquidity with lenders, as all the banks already keep a higher than required amount under SLR. The only difference would be that the banks will raise lesser money for meeting their LCR requirements,” said Ashish Jalan, assistant vice president at SPA Securities.

Talking to reporters, the RBI governor also said it has been decided that non-deposit taking systemically important non-banking financial companies (NBFCs-NDSI) in the category of Investment and Credit Companies (ICCs) will be made eligible to apply for Authorised Dealer Category II licence.

The decision has been taken with a view to improve the ease of undertaking forex transactions by increasing the last-mile touch points of regulated entities to sell foreign exchange for non-trade current account transactions.

A detailed instructions in this regard would be issued by the end of April 2019, he added.

Globally, residential and commercial mortgages are supported by well-lubricated securitisation markets whereby mortgage originators package portfolios of mortgages and resell them in capital markets as mortgage-backed securities or covered bonds.

Well-functioning securitisation markets can enable better management of credit and liquidity risks on the balance sheets of banks as well as non-bank mortgage originators and, in turn, help lower the costs of mortgage finance in the economy.