Question: An individual taxpayer owns a residential house property which was originally purchased in FY2011-2012 for Rs 75 lakh and further renovation cost was incurred in FY2014-15 for Rs 15 lakh. Kindly guide on the amount of capital gains chargeable to income tax if the said residential house property is sold in FY2024-25 for a consideration of Rs 2.5 crore and a brokerage expense of Rs 60,000 was incurred by the taxpayer.

Answer given by Dr. Suresh Surana, Founder, RSM India: The provisions of the Income Tax Act, 1961 (herein after referred to as ‘IT Act’) provides that any income, in the nature of profit or gains, arising on account of transfer of a capital asset shall be chargeable to tax under the head “Capital Gains”.

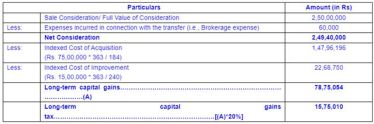

As such, tax on the capital gains shall be computed in accordance with Section 48 of the I-T Act, by deducting from the full value of the consideration received or accruing as a result of the transfer of the capital asset the expenditure incurred wholly and exclusively in connection with such transfer, cost of acquisition of the asset and cost of any improvement thereto.

Also Read: Tax Planning for FY2024-25: Where to invest to save taxes and get higher returns?

Further, in case the capital arises from transfer of a capital asset which has been held for long term, the taxpayer to whom such capital gains pertains, shall be eligible to claim the benefit of indexation with respect to cost of acquisition and cost of improvement.

As per section 2(42A) of the I-T Act, gains derived from any immovable property held for a period of up to 24 months shall be classified under short-term capital gains, otherwise long term. Since in the given case, the taxpayer held the residential house property for a period of more than 24 months, such capital gains would be long term in nature and accordingly, shall be computed after considering the indexation benefits.

Such indexation benefit is computed based on the cost inflation index pertaining to each financial year which is notified by the Income Tax department from time to time. As such, recently the CBDT vide Notification no. 44/2024 dated 24th May, 2024, notified the Cost Inflation Index (CII) for the FY 2024-25 at 363.

The aforementioned capital gains tax amount would be further enhanced by Cess @ 4% and the applicable surcharge, if any.

This Q&A series is published every week on Thursday.

Disclaimer: The views and facts shared above are those of the expert. They do not reflect the views of financialexpress.com