Despite the second wave, Sobha clocked ~0.9msf pre-sales in Q1FY22 (up 38% y-o-y, down 33% q-o-q); its share in new sales was Rs 5.7 bn (+45% y-o-y/-35% q-o-q). Net debt edged down to ~Rs 28.2 bn (Rs 28.5 bn in Q4FY21). Management indicated launches are likely to pick up and the company will continue to focus on cash flow management to reduce net debt: equity (currently 1.15x).

We expect buoyancy in sales to sustain riding revival in housing demand and Sobha’s robust ~12.6msf launch pipeline. Retain Buy with a revised TP of Rs 709/share (Rs 574 earlier) factoring in a reduction in WACC, removal of NAV discount and a valuation rollover to Dec-22e.

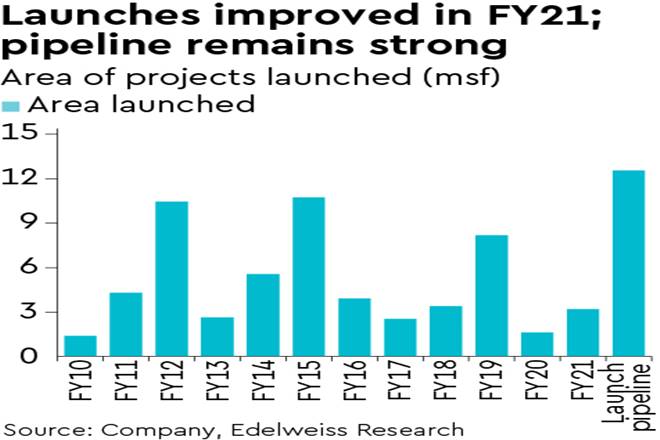

Sales resilient despite second wave

During Q1FY22, the company reported new sales of ~0.9msf with sales volume growing y-o-y across major cities such as Bengaluru, Pune, Gurugram, and Kochi; sales in Bengaluru recovered 37% y-o-y (down 26% q-o-q). Other cities that reported strong y-o-y growth include Pune (165% y-o-y), Gurugram (119% y-o-y) and Thrissur (95% y-o-y). There were no formal project launches during the quarter; the company has a robust launch pipeline of ~12.6msf projects over the next four–six quarters. It expects to launch projects in Bengaluru, Chennai and Gujarat soon.

Debt reduction continues

Aided by healthy collections (up 31% y-o-y), the company managed to reduce its net debt q-o-q to Rs 28.2 bn in Q1FY22. Cash flows were aided by minimal land-related payments. Mgmt indicated it is committed to cash flow management going ahead and hence land-related capex will remain contained (~Rs 0.75-0.80 bn annually). Incremental land acquisition will be funded through internal accruals. Along with project launches, free cash flow and debt repayment will be the key focus areas. It is targeting to bring down net debt:equity to 1–1.1x.

Outlook: Cash flows paramount

With demand recovering and launches likely to pick up, we believe Sobha’s focus on cash flows will hold it in good stead. We continue to follow the old AS and maintain ‘BUY/SN’ with a revised TP of Rs 709/share (on a par with its

NAV of Rs 661/share for the realty business and adding Rs 47/share for contractual business).