Zomato’s food delivery business’ gross merchandise value (GMV) growth came in at 21/1% y-o-y/q-o-q and missed estimates. MTUs were 1% lower q-o-q, amid a weak demand environment afterDiwali. Lower customer acquisition resulted in significantly better-than-expected contribution margins (CM) of 5.1% versus 4.5% in Q2FY23. Lower losses in the core business and Blinkit drove consolidated Ebitda loss of Rs 3.7 bn versus expectations of Rs 4.6 bn. We expect Zomato Gold to be margin dilutive in the near term, though this should boost growth over the medium term. We bake in higher FY2024-25 loss estimates in the core business.

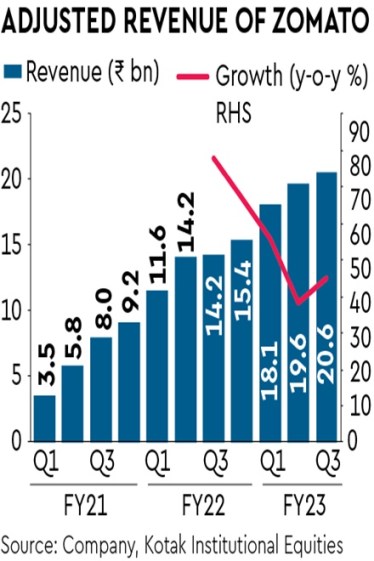

Zomato’s food delivery gross order value (GOV) growth of 21/1% y-o-y/q-o-q was driven by growth in orders (14% y-o-y) and average order value (AOV) (6% y-o-y). Revenue growth of 29% y-o-y outperformed GOV growth of 21% y-o-y due to higher AOVs. We reckon that AOVs have been holding up at Rs 405+ aided by premiumisation and food inflation. Restaurant take-rate of 17.2% in Q3 inched up, but was partially offset by lower customer delivery take-rate of 6.2% (versus 6.7% in Q2). Tepid macro demand led to weaker-than-expected growth of GOV, revenue and MTUs (down 1% q-o-q). Zomato expects restaurant take-rates to inch up further.

The contribution margin increased to 5.1% in 3QFY23 (versus 4.5% in 2Q) and beat expectations. Our analysis shows that higher AOVs and lower costs per order aided CM, offsetting the impact of lower customer delivery charges. Zomato has made considerable progress in containing losses of the core business. Adjusted Ebitda loss was lower-than-expectations at Rs 3.7 bn in 3Q (versus KIE estimate of Rs 4.6 bn), led by higher CM of food delivery business and lower-than-expected loss in Blinkit.

Blinkit’s GOV grew 18% q-o-q, driven by a 21% q-o-q in orders, offsetting lower AOV. Better monetisation-led higher revenue per order led to revenue growth of 28% q-o-q. Dark store footprint declined for the quarter, as some short-term contract s expired. Dark store count is expected to increase at a calibrated pace. Profitability continued to improve, with CM improving from (-)7.3% in 2Q to 4.5% in 3Q. Adjusted Ebitda loss decreased from Rs 2.6 bn in 2Q to Rs 2.3 bn. Zomato indicated that Blinkit gained share versus next day/week ecommerce businesses (Amazon, Flipkart).

We revise down FY2023 food delivery GMV owing to the 3Q miss and possibly no major improvement in 4Q. Additionally, we tinker near-term margins, as we bake in the impact of Zomato Gold.