Headline revenue growth of 23% y-o-y (7th consecutive quarter of 20%+ growth) with ex-Lloyd growth of 28%

y-o-y was commendable. Switchgears, Cables/wires and ECD grew strong at 28/35/42%. Lloyd de-grew 5% y-o-y on adverse seasonality and higher channel inventory. Revenue trajectory remains intact on a good start to the festive season.

Contribution margin deteriorated in all but the lighting segment. A lag in passing on the costs from depreciating INR, commodity costs led to margin compression (Cables/wires and Lloyd segments). This will be recouped in the forthcoming quarters. Improved product mix aided margin in lighting despite declining LED prices.

A&P expenses, while higher in Q2, to remain at 3% of revenue going forward. Capex in FY19 (including new RAC plant) would be Rs 5 bn; regular capex post that would be reduced to Rs 2 bn driving RoCEs/FcFF generation.

Our viewHavells has established itself as a market leader across categories, being at the forefront of innovation with several ‘industry-firsts’ in the past (premium fans, channel financing, IoT-enabled devices etc.).

This has enabled steady premiumisation trends. Investing in brand, people and distribution has enabled it to go ‘deeper into homes’ and be among top 3 players in most segments. In-house manufacturing/design enables significant control on quality of output, giving it an edge. Individual SBU efforts and focus on cost management and profitability are playing out.

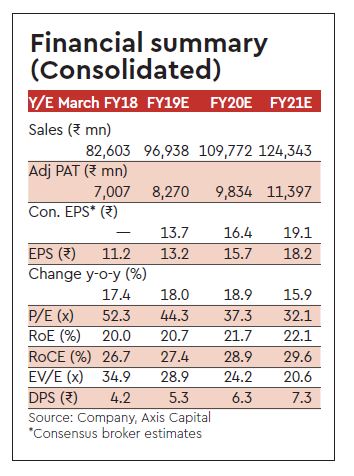

With continued focus on innovation, brand building, and distribution, we expect HAVL to post 15/18% CAGR (FY18-21) on revenue/PAT, with RoCEs improving to 30%. Given the growth/ margin/ROCE profile, we believe a valuation at 37x FY20 P/E is pricy. We trim our estimates to factor in weaker Q2 performance and roll forward our TP to Rs 560 (implied multiple of 33x Sept 20 P/E) from Rs 570 earlier.

Hold Segment-wise break-up

Switchgears: Revenue at Rs 4.2 bn grew 28% y-o-y. Industrial switchgears have grown faster this quarter. Despite strong headline numbers, contribution margin declined ~300 bps y-o-y to 38.5%.

Cables and wires: Revenue grew 35% y-o-y led by 20% volume growth; however contribution margin at 14% reported a sharp decline of 600 bps y-o-y.

Lighting and fixtures: Revenue at Rs 2.9 bn was flat y-o-y despite continued price erosions in LEDs. Contribution margin at 29.6% improved 260 bps y-o-y.

Electric consumer durables: Revenue at Rs 4.6 bn grew 42% y-o-y, largely driven by fans (both premium and base categories). Contribution margin at 27.3% contracted ~50 bps y-o-y.

Lloyd: Revenue at Rs 2.6 bn de-grew 4% y-o-y on seasonality and higher channel inventory during the quarter. Contribution margin at 18.5% declined 100 bps y-o-y on forex headwinds and delay in passing on these adversities to the end consumer in form of price hikes.