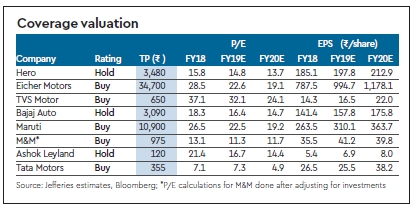

Volume growth has been divergent across segments and OEMs in Q2FY19e with Ashok Leyland, Bajaj and TVS expected to deliver 20%+ revenue growth and single-digit growth for others, partly on account of a delayed festive season. We expect Ebitda margin to be down y-o-y across the board putting further pressure on profits, with Ashok Leyland likely the only exception. Commentary on festive season demand (Oct/Nov) and margin outlook for H2 will be key to look out for.

Hero (Hold): After four quarters of double-digit volume growth, Q2 has been relatively weak for Hero with growth decelerating to 5% partly on account of a delayed festive season. We expect Ebitda margin to be down 200bps y-o-y.

Eicher (Buy): Q2 will be a first for Eicher as volume growth has decelerated to single-digits for the first time in many years. We expect weaker operating leverage and raw material cost pressures to have some adverse impact on margins as well.

TVS (Buy): We expect TVS to report 20%+ revenue growth but despite resultant operating leverage benefits, Ebitda margin is likely to be down 50bps y-o-y.

Bajaj Auto (Hold): Bajaj Auto has reported 25% volume growth in Q2 but as in Q1, margin will be key given its aggressive pricing strategy. We expect Ebitda margin to be up marginally q-o-q.

Maruti Suzuki (Buy): We expect Ebitda to be down 14% y-o-y due to weak volume growth (-1% y-o-y) and sharp margin contraction (270bps). A combination of factors will weigh on margin.

M&M (Buy): Volume growth has been weak for M&M in Q2 with tractors down 4%, PVs down 7% and CVs up 24%. We expect margin to be weaker y-o-y and q-o-q.

Ashok Leyland (Hold): Ashok Leyland has delivered the biggest positive surprise on growth in Q2 especially in the context of uncertainty related to the new axle norms. We expect 27% volume growth to lead to a similar revenue growth, 40% Ebitda growth and 50% net profit growth y-o-y.

Tata Motors (Buy): Turnaround of Tata Motors’ standalone business remains on track with Q2 Ebitda expected to be up sharply y-o-y and positive net profit vs losses last year. However, fundamentals for JLR have deteriorated materially and will lead to a sharp decline in consolidated Ebitda.